Paid, Planted, and Silenced: How a Named Review Farm Is Running Unchecked Across India's Top Fintech Apps

InvestigationSix Apps · 15,000+ ReviewsFiled 1–3 July 2026 Read this first On 1 July 2026, a user named ABHINAV left…

A single afternoon of research uncovered a coordinated fake-review campaign on a live fintech lending app. Here is what I found, how it works, and what you should do before trusting any star rating.

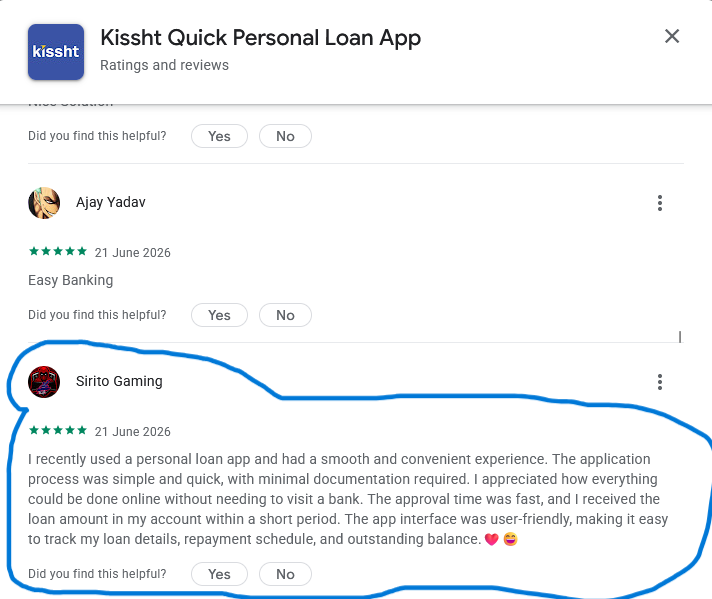

Look at these two screenshots. Different names. Different profile pictures. Same review. Word for word. Emoji for emoji.

Two different names. Two different profiles. One script.

Sahaj RAJPUROHIT and Sirito Gaming are supposedly two separate people who both downloaded the same personal loan app, had the exact same experience, and independently decided to describe that experience using identical sentences, identical punctuation, and identical emojis.

That did not happen.

What you are looking at is manufactured social proof, running live on Google Play, on a financial lending app. I found this while cross-referencing app reviews for research on my platform. I kept scrolling. I found more. A lot more.

This post documents exactly what I found and tells you how to protect yourself before you download any financial app based on its star rating.

Before I get into the evidence, I want to be direct about why this matters more than fake reviews on a food delivery app.

If a restaurant has fake 5-star reviews and you end up with bad food, you lose a few hundred rupees and a couple of hours. Annoying, not dangerous.

A personal loan app is different. People who download loan apps are often already under financial pressure. They are looking for quick relief. They are making a decision that can affect their credit score, their bank account, and their financial stability for months, sometimes years.

If they download a predatory or poorly structured lending app because it had a 4.5-star rating, the consequences are not a bad meal. I have written about this specifically in the context of whether instant loan apps are actually safe in India. The short answer is: it depends heavily on verification, and a Google Play rating tells you nothing about that.

The fake reviews I am about to show you were on a live, active fintech app with thousands of downloads. Google Play published every single one without a flag, a warning, or a removal.

I am not asking you to take my word for it. Here is the evidence, broken into five distinct patterns I identified across a single app’s review section, collected on a single day.

The most obvious form of review manipulation is direct duplication. Write one review, post it from multiple accounts.

A basic plagiarism check would have caught this in seconds. Google Play published both.

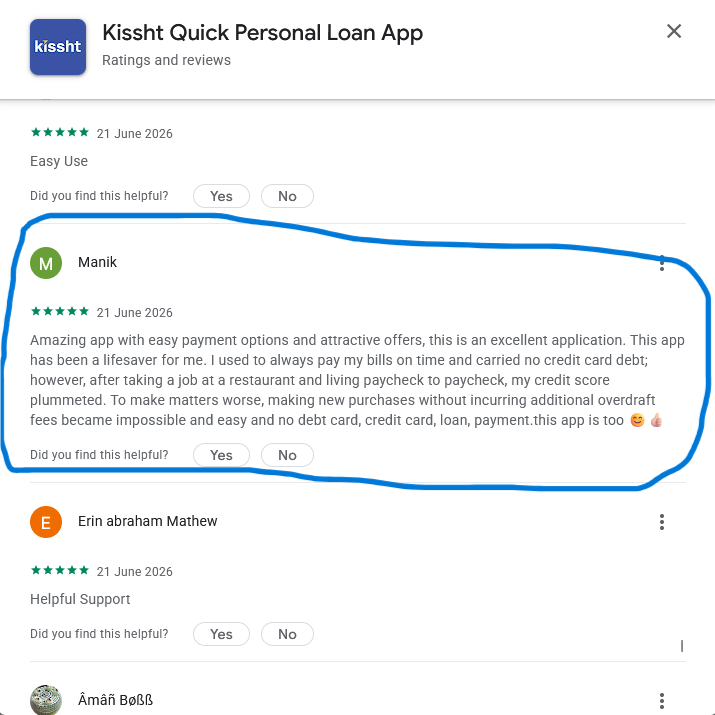

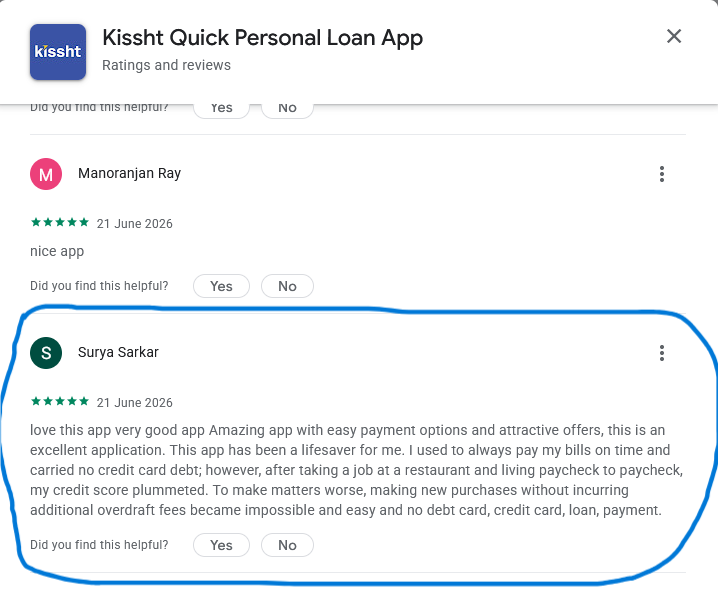

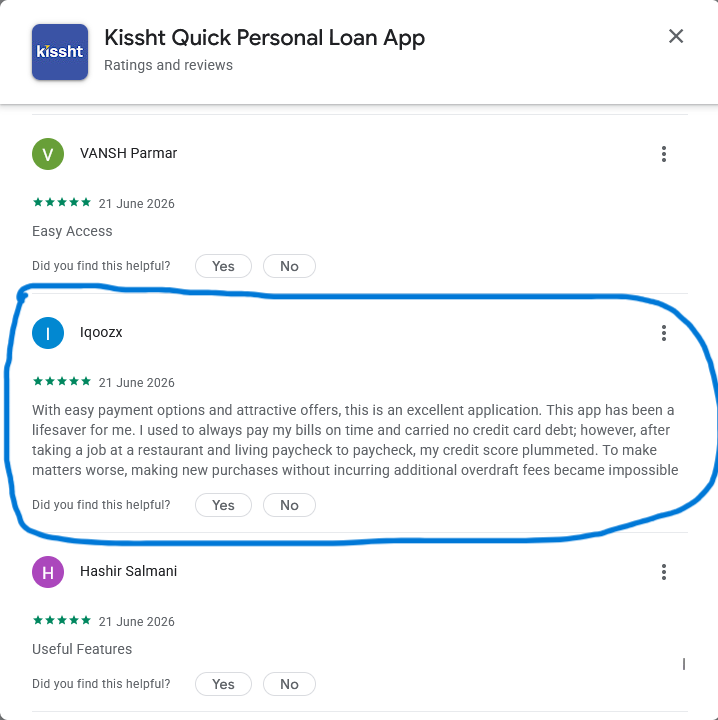

This is where it gets more sophisticated, and more revealing about how these operations actually work.

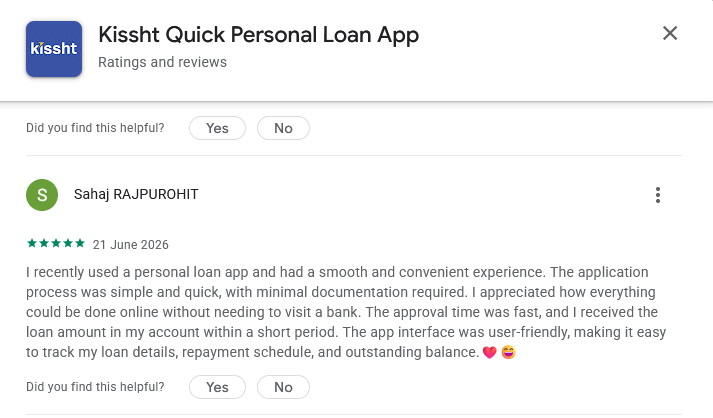

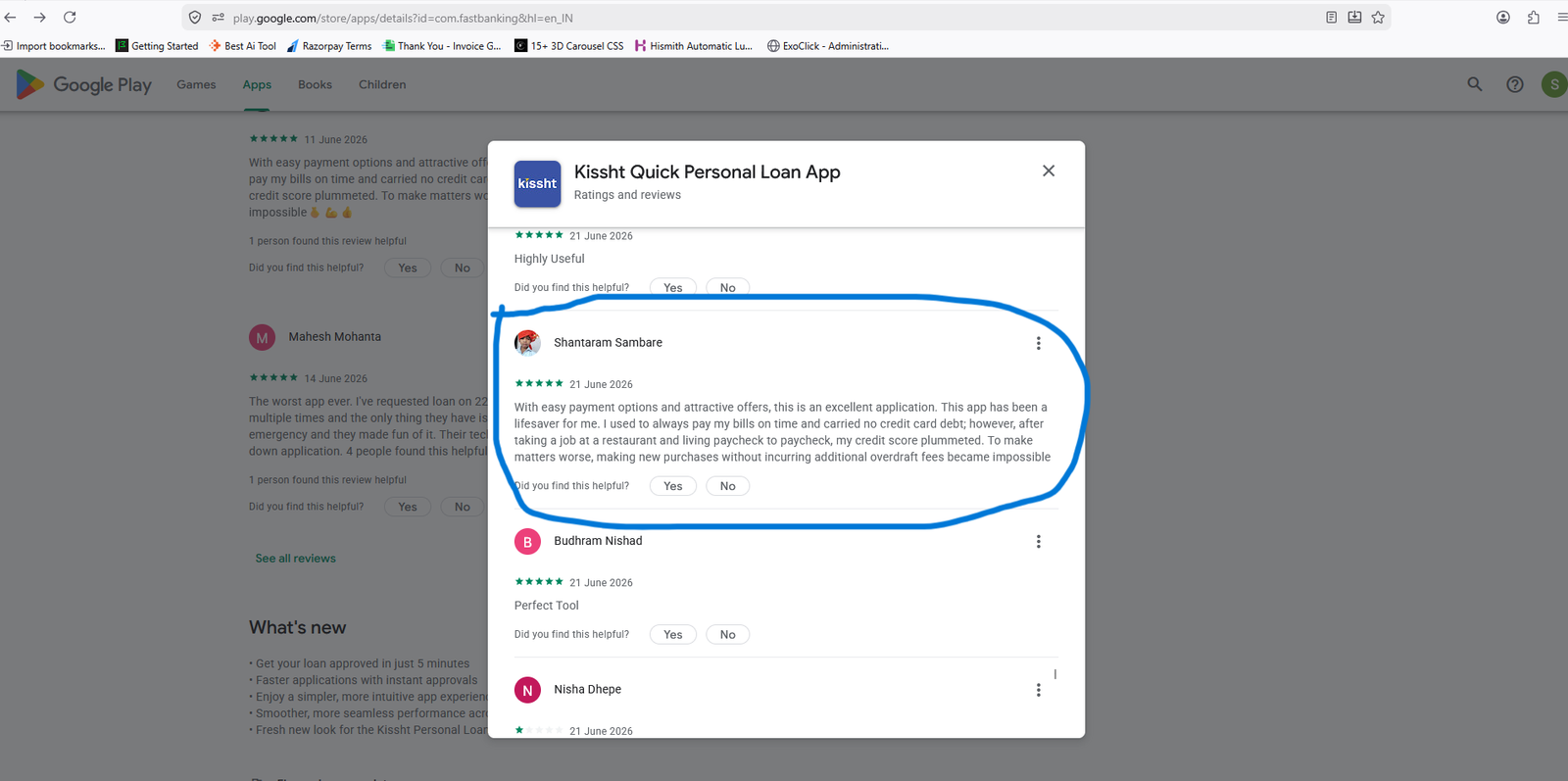

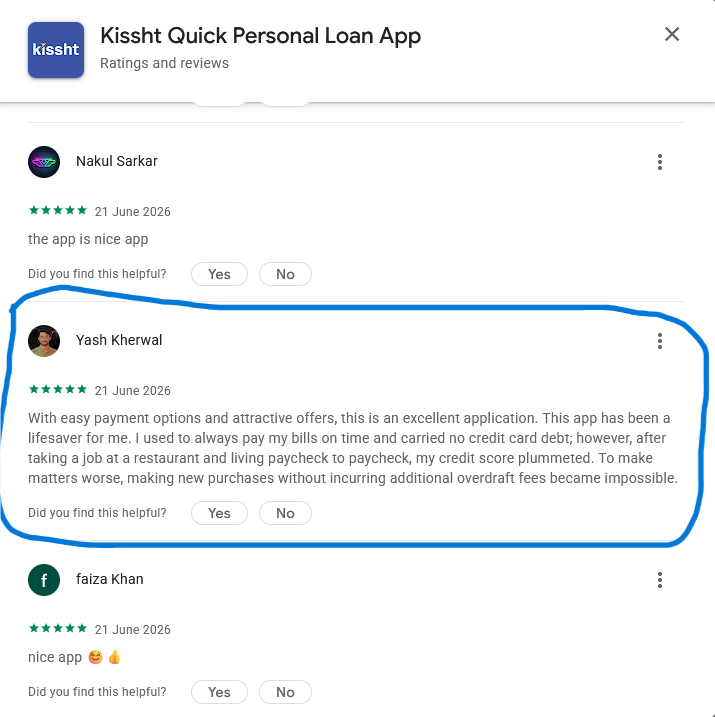

A single core paragraph is written once. It is then distributed across dozens of accounts. Each account adds a slightly different opening or closing sentence to fool basic duplicate-detection filters. The result is reviews that are 90 to 95 percent identical but technically not exact copies.

The planted story across multiple accounts goes like this: a person takes a restaurant job, starts living paycheck to paycheck, their credit score plummets, they discover the app and it saves them. The financial hardship angle is deliberate. It is written to create emotional resonance with readers who are themselves under financial stress, the exact people most likely to be searching for a loan app.

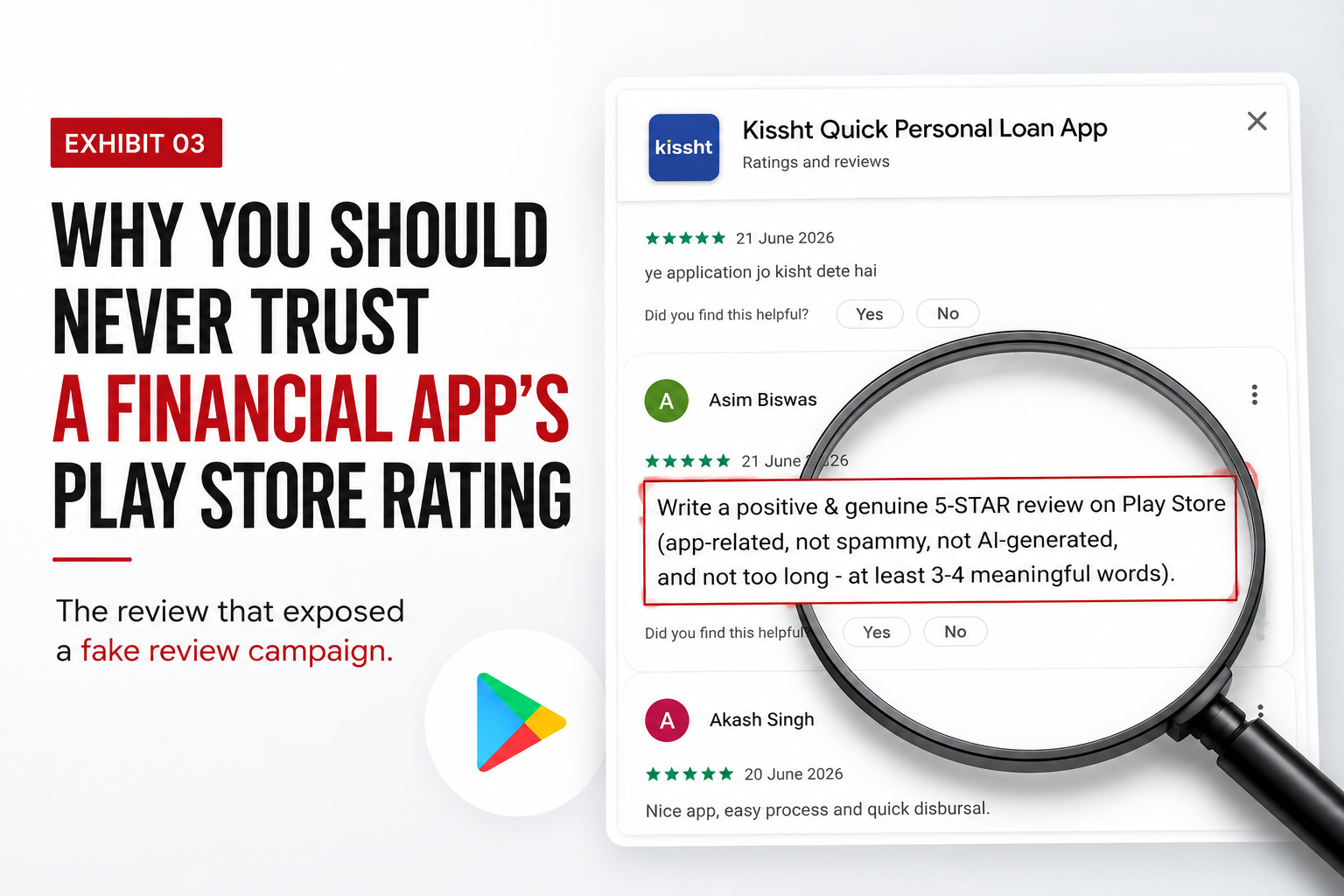

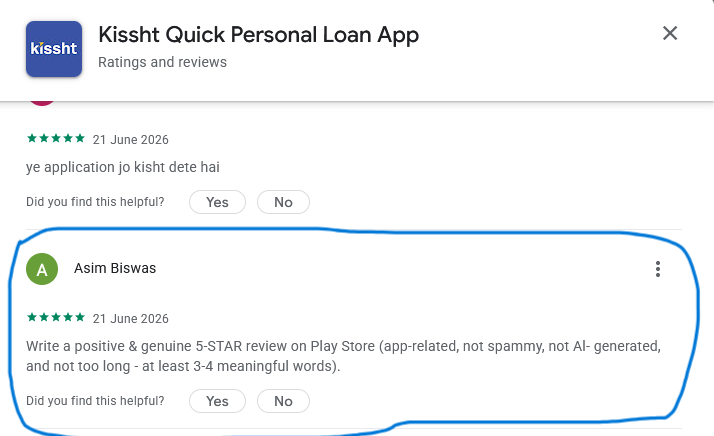

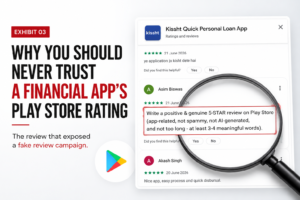

This is the most extraordinary piece of evidence I found. It removes every remaining doubt about what is happening here.

The user “Asim Biswas” did not leave a review. He accidentally published the task brief he was given. The text reads: “Write a positive and genuine 5-STAR review on Play Store (app-related, not spammy, not AI-generated, and not too long, at least 3-4 meaningful words).”

That is the operating instruction for a paid review campaign. The worker forgot to replace the prompt with the actual review. This sat on Google Play’s review section, publicly visible, and was never removed.

This is not speculation about review fraud. This is the instruction manual for review fraud, submitted as the review itself.

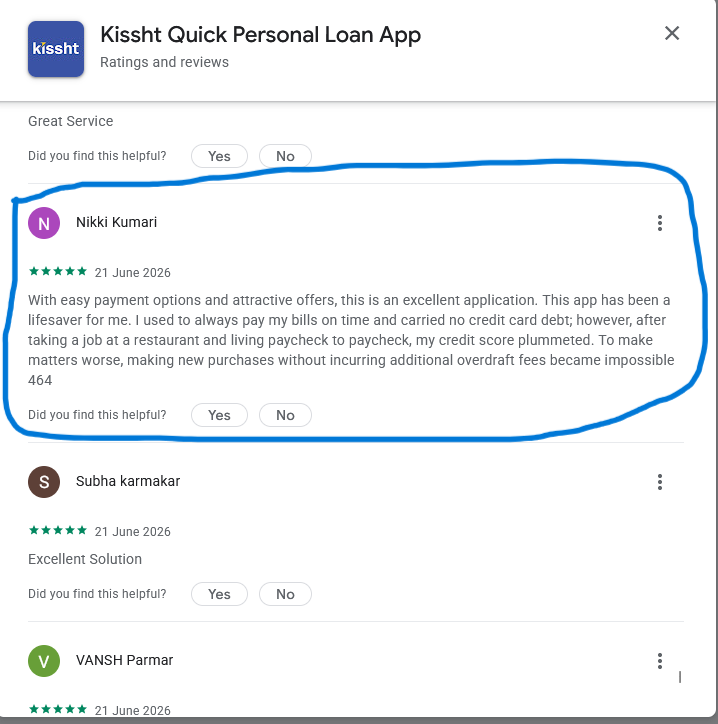

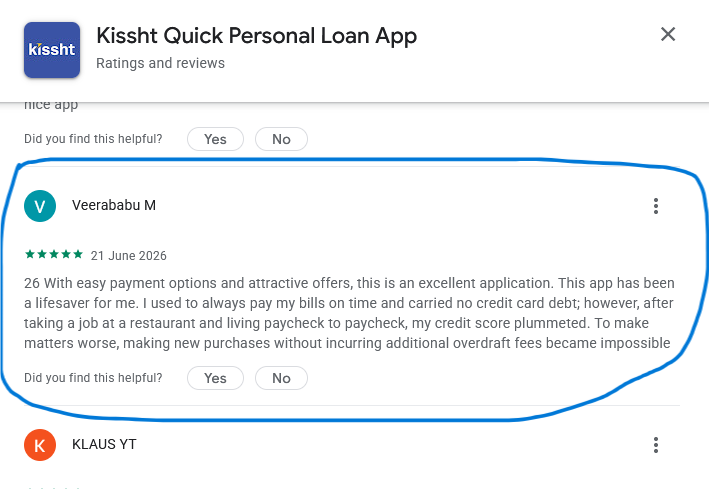

Bots and low-wage review workers using pre-filled scripts leave traces. The most common trace is a random number or stray character string at the start or end of a review, a leftover from a script variable that was never cleaned before the text was submitted.

“Nikki Kumari” ends her review with the number 464. “Veerababu M” begins his review with the number 26. Neither number has any logical connection to what they wrote. These are production errors left behind by automation, the same kind of error you see when a mail merge fails and a letter reads “Dear [FIRST NAME]” instead of a real name. Automation ran, and nobody checked the output.

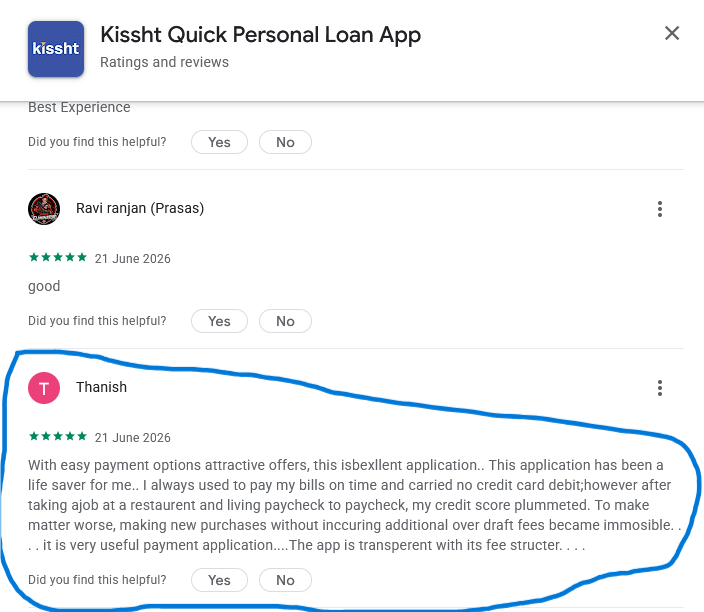

The final fingerprint is a profile that has no business writing the review it posted.

Look at the profile picture. Now look at the review content: a job at a restaurant, a falling credit score, growing overdraft fees. That is not the financial profile of the person in that profile picture.

This is either a purchased account, a stolen account, or a junk profile handed to a worker with one instruction: post this text. The account has zero plausible connection to the content it submitted. Google Play published it without question.

Every single screenshot in this post carries the same timestamp: 21 June 2026.

This was not an organic accumulation of satisfied customers leaving feedback over several weeks. This was a coordinated campaign, executed across dozens of accounts, on a single afternoon. The entire operation ran without a single flag, a single removal, or a single intervention.

When a platform allows the instruction slip of a paid review campaign to sit publicly on a page that tens of thousands of users may visit before downloading a lending app, calling it a moderation system is too generous.

I want to be precise here, not unfair. Google Play handles a volume of content that no human team can fully review manually. Scale is a real constraint, and I acknowledge that.

But understanding scale does not mean accepting its consequences as normal, especially when the platform in question is being used by people making financial decisions.

Three structural problems are worth naming directly.

First, a star rating is a number, not a verification. A 4.5-star rating tells you that accounts submitted positive text to a database. It tells you nothing about whether those accounts belong to real people, whether those people actually used the app, or whether the app itself is registered, regulated, or operating within legal boundaries.

Second, for financial apps in particular, there is a verification gap that no rating system fills. Before recommending any lending service, I point readers to the list of RBI-approved loan apps in India with trust scores I maintain on TrustGate. A regulatory approval is a real signal. A star count is not.

Third, the incentive structure of app store platforms does not urgently demand the kind of verification that would reduce download numbers. I am not making an accusation. I am pointing out a structural misalignment that consumers need to account for when they use a star rating as a safety signal.

The goal of this post is not just to show you a problem. Here is the practical response to it.

Copy any paragraph from the app’s glowing reviews and paste it into Google Search with quotation marks around it. If the same sentence returns results under multiple different names across multiple platforms, it is templated content from a distribution campaign. The restaurant and credit score paragraph from this post alone would return dozens of matches.

Sort reviews by “Most Recent” and look at the posting dates. If you see fifteen or twenty 5-star reviews all posted on the same day, followed by a gap of several weeks, you are looking at a campaign, not organic feedback. Real user reviews accumulate gradually and unevenly. Coordinated campaigns spike and go quiet.

Negative reviews are significantly harder to fake. The people leaving 1-star and 2-star reviews are typically real users who had a real experience bad enough to motivate them to write about it. Read the lowest-rated reviews before you read the highest. They are the more reliable signal.

A star rating says nothing about whether a lender is legally registered or financially regulated. Before downloading any loan app, confirm the company has a real registered address, that it is listed as an NBFC or bank-affiliated lender under RBI guidelines, and that its website has functional contact information. My guide on how to check if a service provider is legitimate in India walks through this process step by step for anyone who wants a structured approach.

Scan reviews for stray numbers or characters at the start or end of review text with no logical connection to what is written. Check whether the profile picture of the reviewer has any plausible connection to the financial context of the review. Look for reviews that begin with near-identical phrasing across multiple accounts. These are not coincidences. They are production errors that survived moderation because there was no meaningful moderation to survive.

The same principles that apply to fake app reviews apply to fake e-commerce platforms. I have covered how to identify fake e-commerce websites in India separately, with a practical framework you can apply immediately.

I built TrustGate because I spent enough time in the Indian digital marketplace to understand that the current system of social proof is broken. Not slightly imperfect. Structurally broken.

The evidence in this post did not come from a weeks-long investigation. I was cross-referencing one app’s reviews for a few minutes. This is what appeared on the surface. Anyone willing to spend an hour on any popular fintech app’s review section will find the same patterns.

A rating is a number that any coordinated operation can manufacture. Verification is a process that requires a real entity to stand behind a real registration with real accountability. Those are not the same thing, and the gap between them is where consumer harm happens.

Before you download any financial app, especially one that will access your bank account, your Aadhaar data, or your credit profile, I would encourage you to start with our best instant loan apps in India for 2026 as a baseline. Every listing on TrustGate goes through a verification layer that a Play Store star rating cannot replicate and was never designed to.

The next time you see 4.5 stars and 50,000 reviews on a lending app, remember the instruction slip that Asim Biswas accidentally posted instead of a review. Remember the restaurant story that appeared across twenty accounts on one afternoon.

Those stars were not earned. They were ordered.

InvestigationSix Apps · 15,000+ ReviewsFiled 1–3 July 2026 Read this first On 1 July 2026, a user named ABHINAV left…

InvestigationTrustgate Field NotesFiled 21–22 June 2026 I am going to say something plainly, and then I am going to prove…

Investigative Report A single afternoon of research uncovered a coordinated fake-review campaign on a live fintech lending app. Here is…