Paid, Planted, and Silenced: How a Named Review Farm Is Running Unchecked Across India's Top Fintech Apps

InvestigationSix Apps · 15,000+ ReviewsFiled 1–3 July 2026 Read this first On 1 July 2026, a user named ABHINAV left…

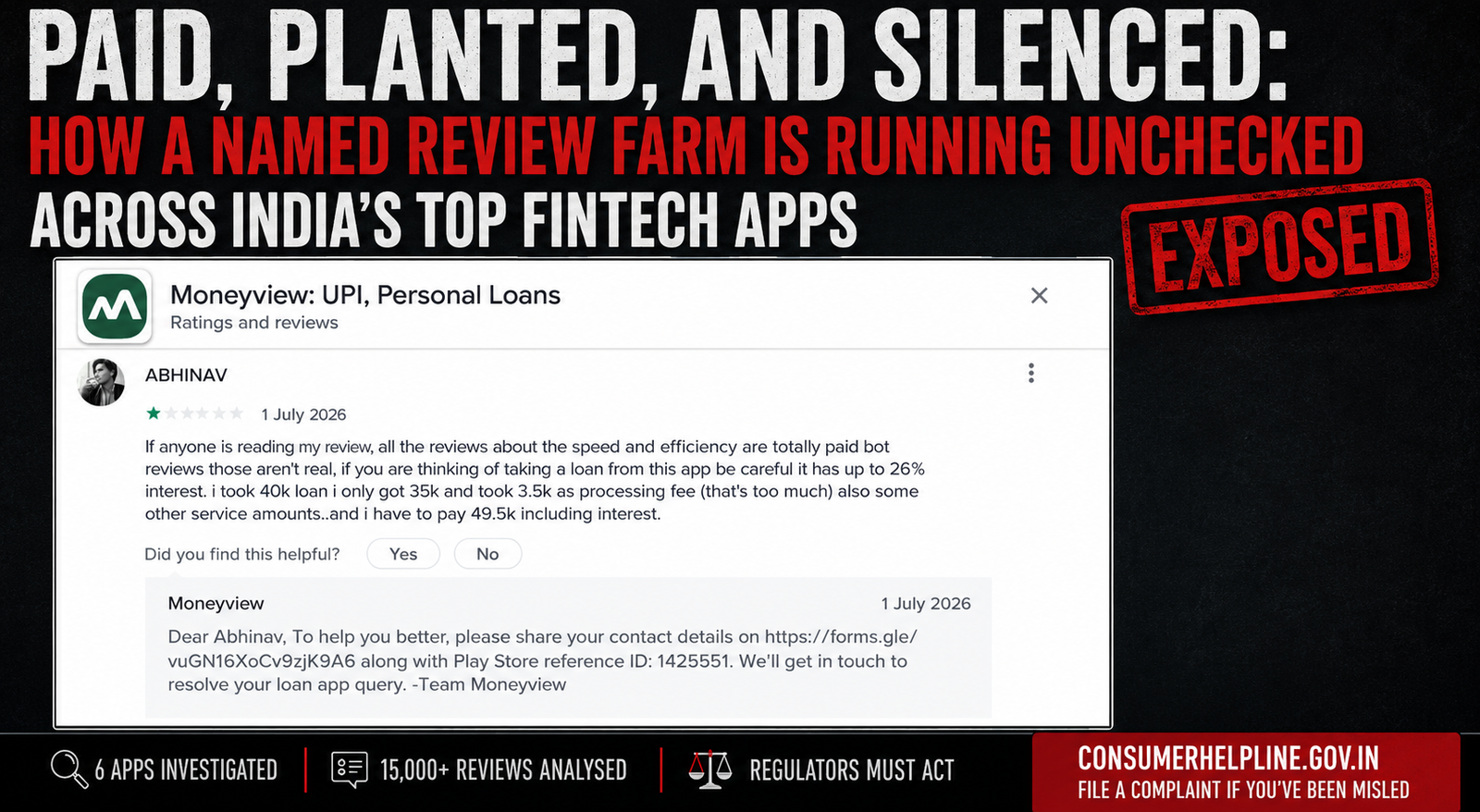

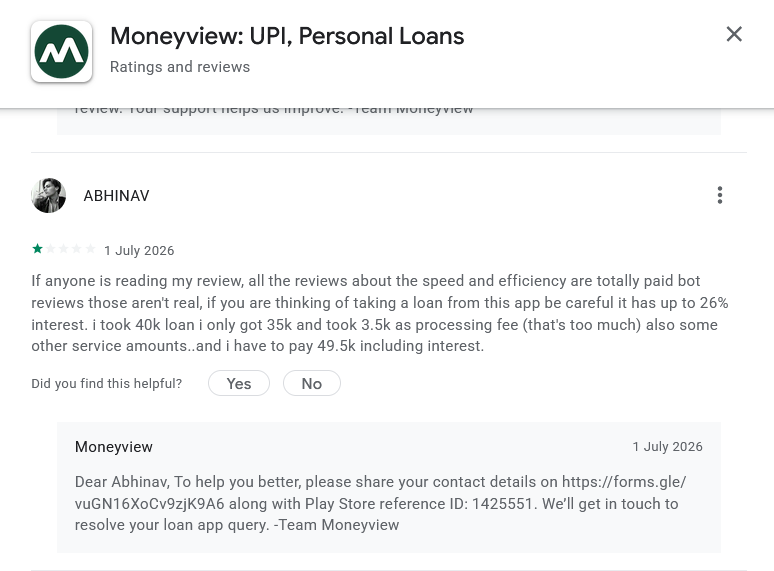

On 1 July 2026, a user named ABHINAV left a 1-star review on the MoneyView app’s Google Play page. He was not reviewing the app’s interface or its customer service response time. He was warning strangers.

“If anyone is reading my review, all the reviews about the speed and efficiency are totally paid bot reviews those aren’t real, if you are thinking of taking a loan from this app be careful it has up to 26% interest. i took 40k loan i only got 35k and took 3.5k as processing fee (that’s too much) also some other service amounts..and i have to pay 49.5k including interest.”

He borrowed 40,000 rupees. He received 35,000 after fees were deducted before the money reached him. He has to repay 49,500.

He read the reviews first. The reviews told him this app was fast, seamless, and built for professionals. They had been submitted by accounts named after referral codes. They were templates.

MoneyView’s official response to his review: “To help you better, please share your contact details on [form link]. We’ll get in touch to resolve your loan app query.”

They did not address his accusation about fake reviews. They asked him for his contact details.

A real borrower, not a researcher. 40,000 borrowed. 35,000 received. 49,500 to repay.

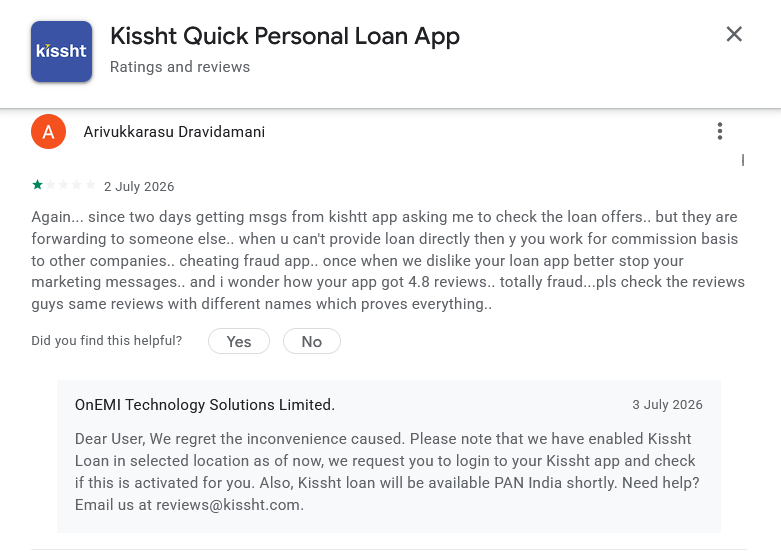

One day later, on 2 July 2026, a user named Arivukkarasu Dravidamani left a 1-star review on Kissht’s Google Play page. He wrote that the reviews were “same reviews with different names which proves everything” and told readers to check for themselves.

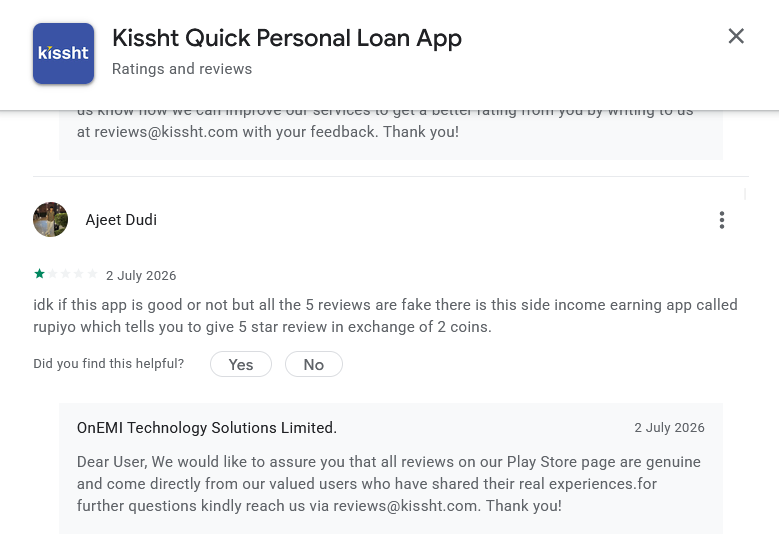

On the same day, a user named Ajeet Dudi left a second 1-star review on Kissht’s page. He went further. He named the specific third-party platform: “there is this side income earning app called rupiyo which tells you to give 5 star review in exchange of 2 coins.”

Kissht’s parent company, OnEMI Technology Solutions, responded officially: “all reviews on our Play Store page are genuine and come directly from our valued users.”

That response was published on the same day as Ajeet Dudi’s accusation, in the same thread, directly below his named allegation. By 3 July 2026, both Ajeet Dudi’s review and Arivukkarasu’s review were gone.

Named the platform. Named the mechanism. Gone within 24 hours.

Three people named the fraud across two apps across two consecutive days. Three company responses ignored the accusation and addressed everything else. Two of the three reviews were removed within 24 hours.

The official denial is still standing.

Section 01 — ScopeI need to be precise about the scope of what I am documenting here, because the scope is the argument.

The Kissht evidence is where this investigation started. I documented it in detail in the first post of this series and in a structural analysis of Google Play’s rating system in the second post. If you have not read those, the short version is this: in a single afternoon in June 2026, more than twenty templated fake reviews were submitted to Kissht’s page on Google Play, including one that accidentally published the campaign instruction brief instead of the review. None of it was caught. All of it was published.

After documenting Kissht, I kept going. I checked Fibe, MoneyView, Navi, Stashfin, and True Balance. I reviewed more than 15,000 individual reviews across six apps. I found the same pattern on every single one.

Different templates. Different farms. Different apps. One platform. One absence of moderation.

The question stopped being whether individual apps run fake review campaigns. That is established. The question is why a platform serving hundreds of millions of Indian users has no enforcement mechanism capable of catching what any individual researcher can find in a single afternoon of scrolling, and why real users who try to warn other users on that platform disappear within 24 hours.

Section 02 — The EvidenceI am not going to repeat the Kissht evidence in full here. You can read it in the first post. What I am going to show you is what the same operation looks like across five additional apps, because the scale is the argument.

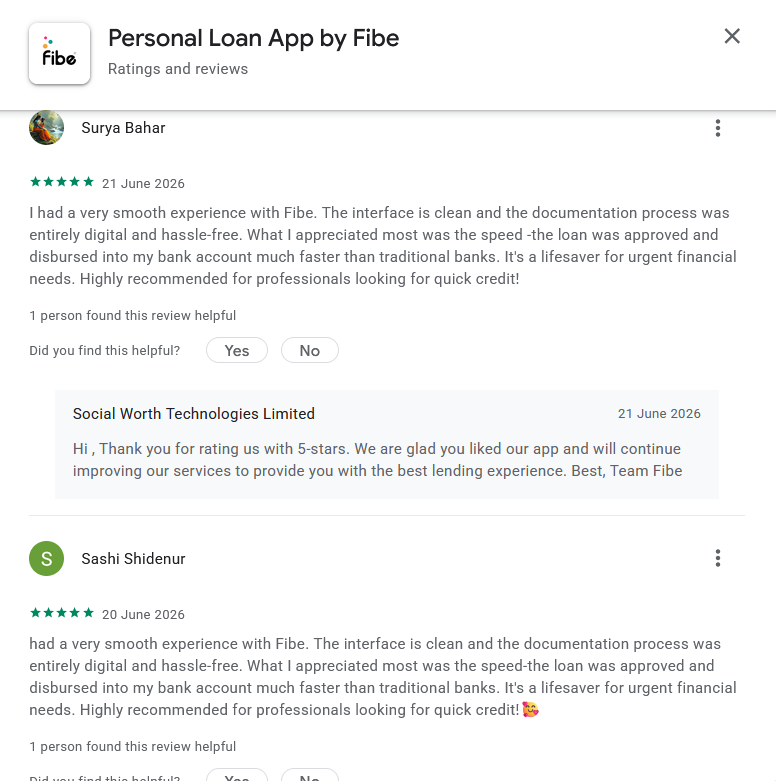

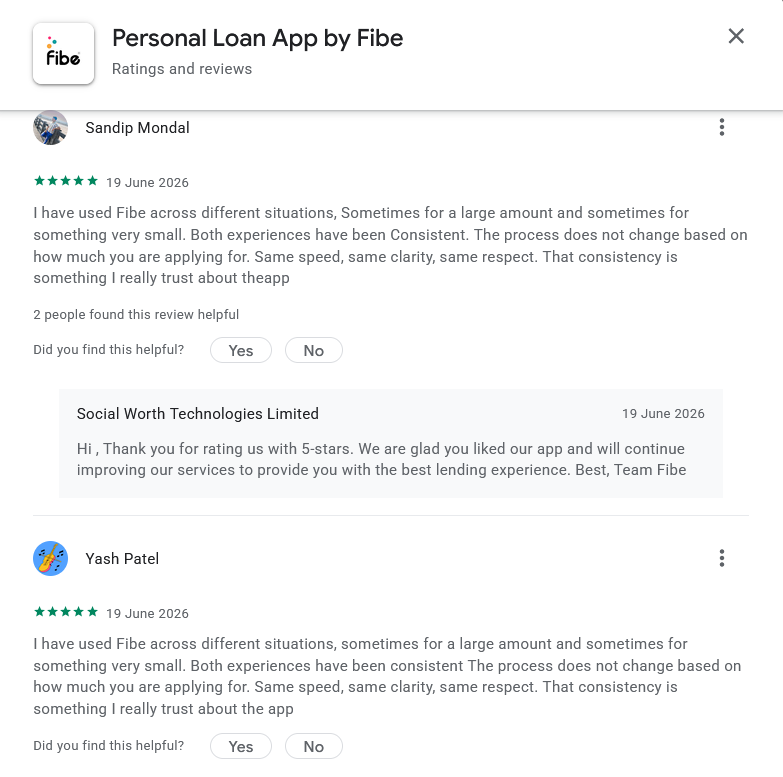

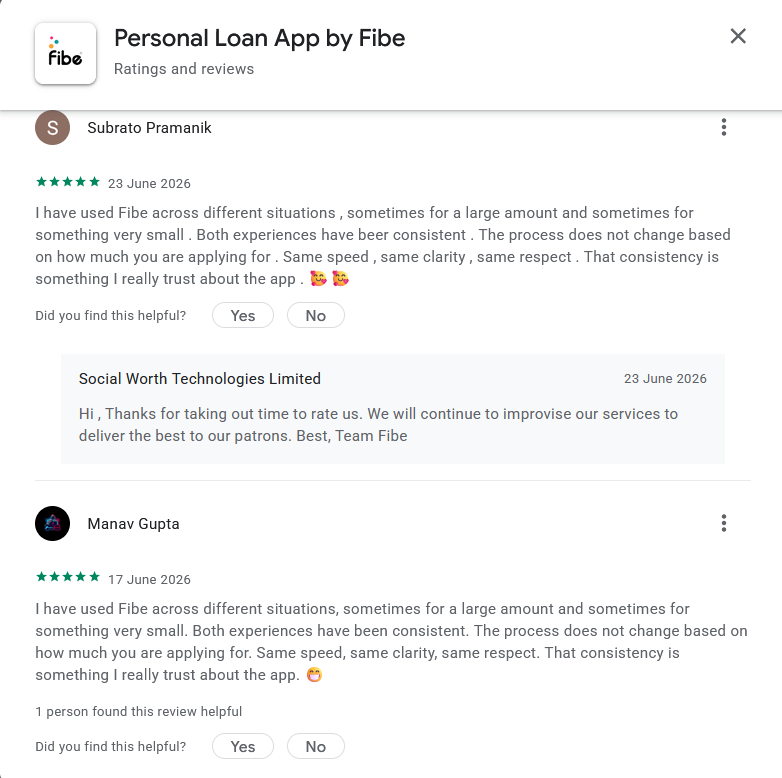

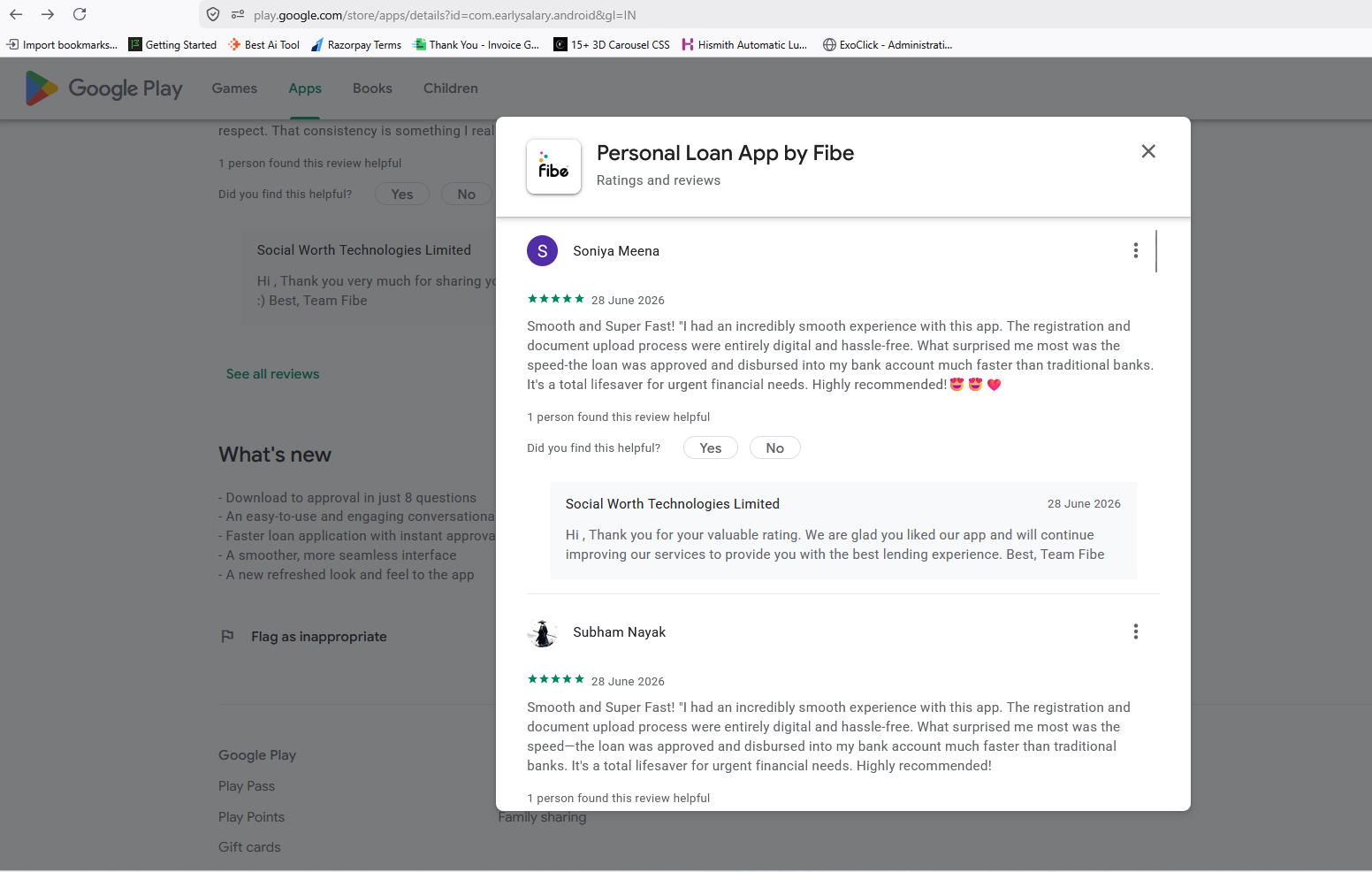

App 01 · FibeFibe’s developer account, operating under the name Social Worth Technologies Limited, personally thanked users for reviews that are word-for-word identical to other submissions on the same page.

Four pairs. Four sets of near-identical wording. The developer thanked all of them.

Surya Bahar and Sashi Shidenur submitted the same review across consecutive days. Sandip Mondal and Yash Patel submitted near-identical reviews on the same day. Subrato Pramanik and Manav Gupta, Soniya Meena and Subham Nayak, the pattern repeats down the page.

When a company’s own team personally thanks users for reviews they claim to have no knowledge of manufacturing, one of two things is true. Either the left hand does not know what the right hand is doing. Or both hands know, and the thank-you is performance.

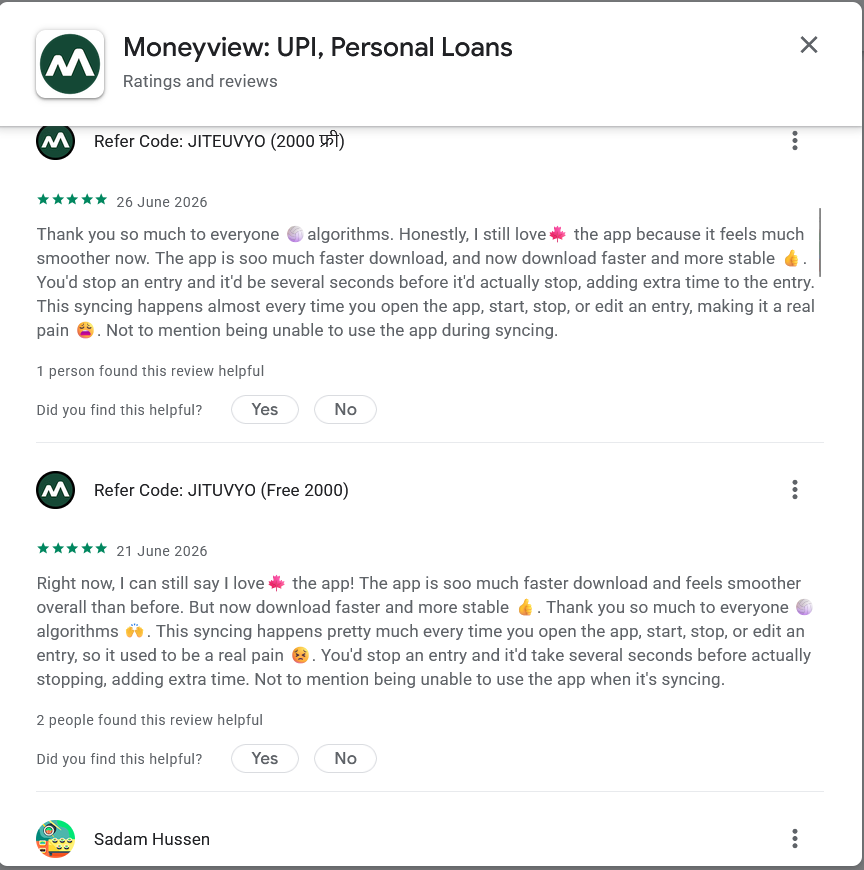

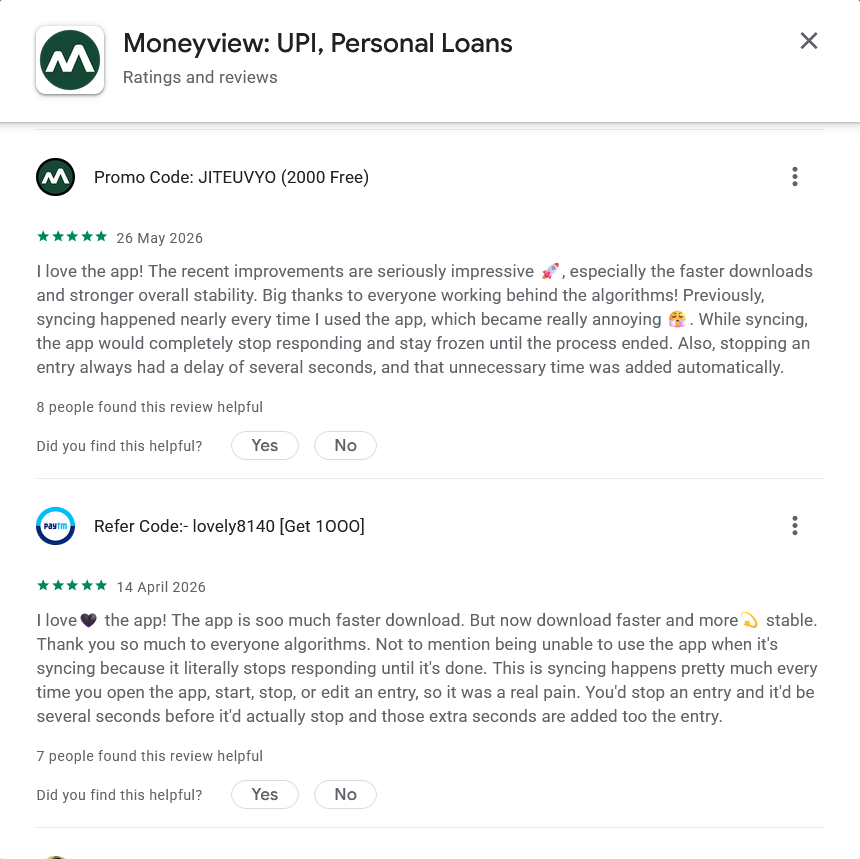

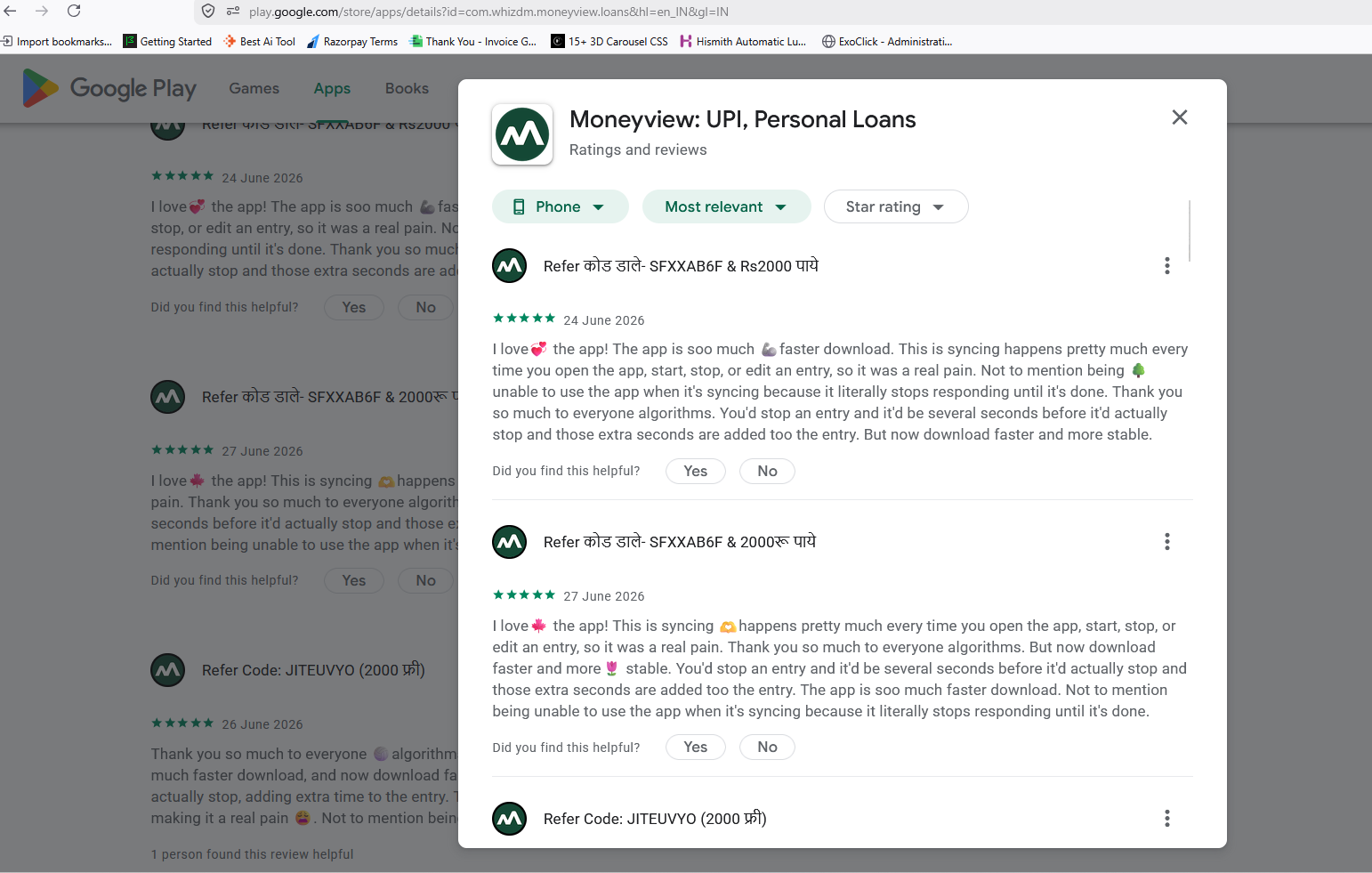

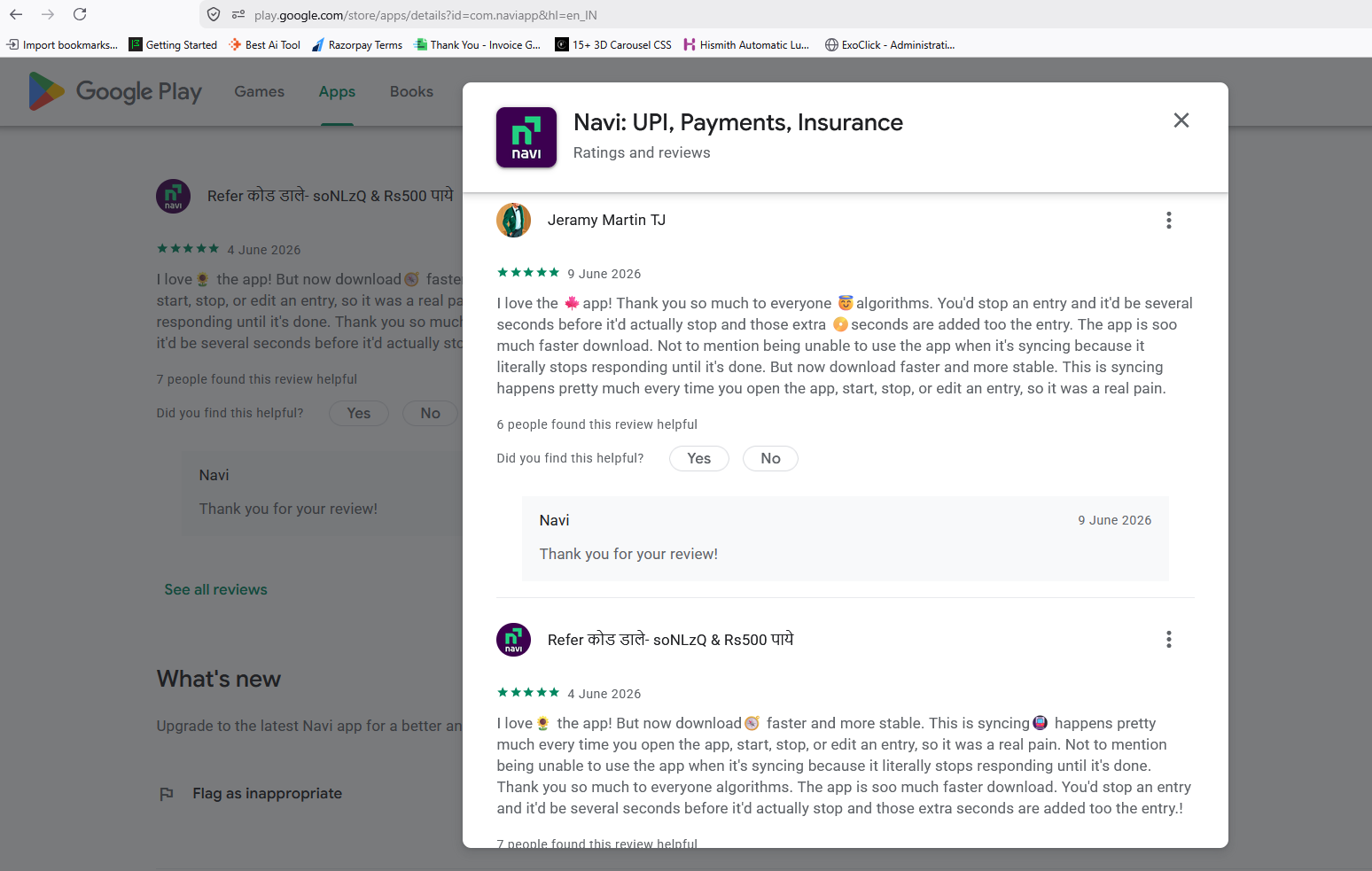

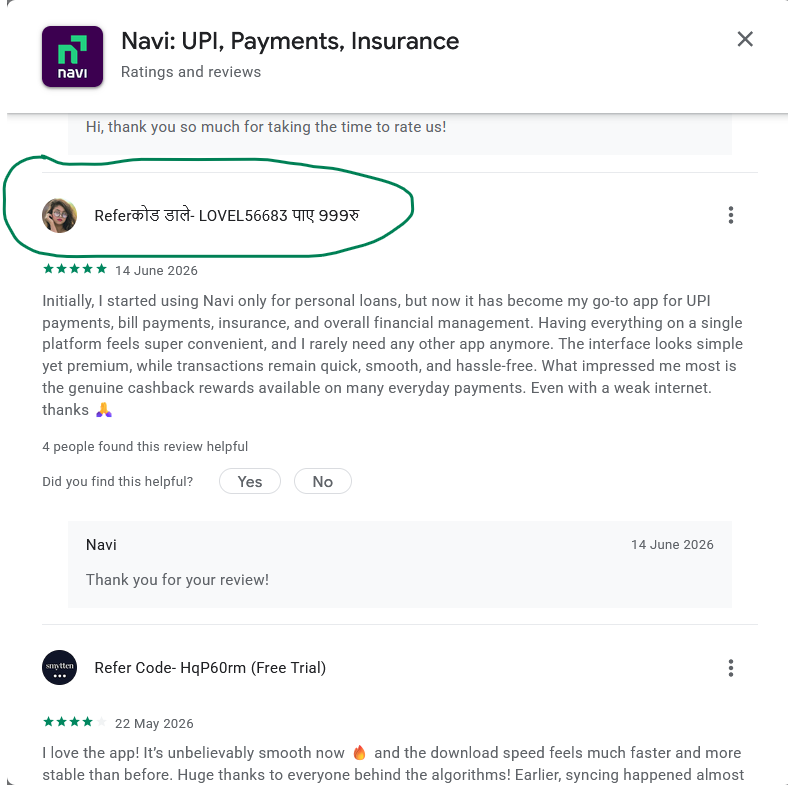

App 02 · MoneyViewMoneyView introduced a category of fraud that did not exist in the Kissht evidence. The accounts posting fake reviews are not using fake personal names. They are named after referral codes and reward amounts. The account name is the payment receipt. The incentive mechanism is printed on the profile.

![Screenshot showing Google Play reviews for the Moneyview app by Dildar Hossain and the profile Refer Code: lovely8140 [Get 1000] containing closely matching review wording.](https://trustgate.in/wp-content/uploads/2026/07/moneyview-google-play-review-dildar-hossain-lovely8140-get-1000-duplicate-reviews.png)

Refer Code: JITEUVYO. Refer कोड डाले SFXXAB6F. Refer Code lovely8140. The reward amount is the username.

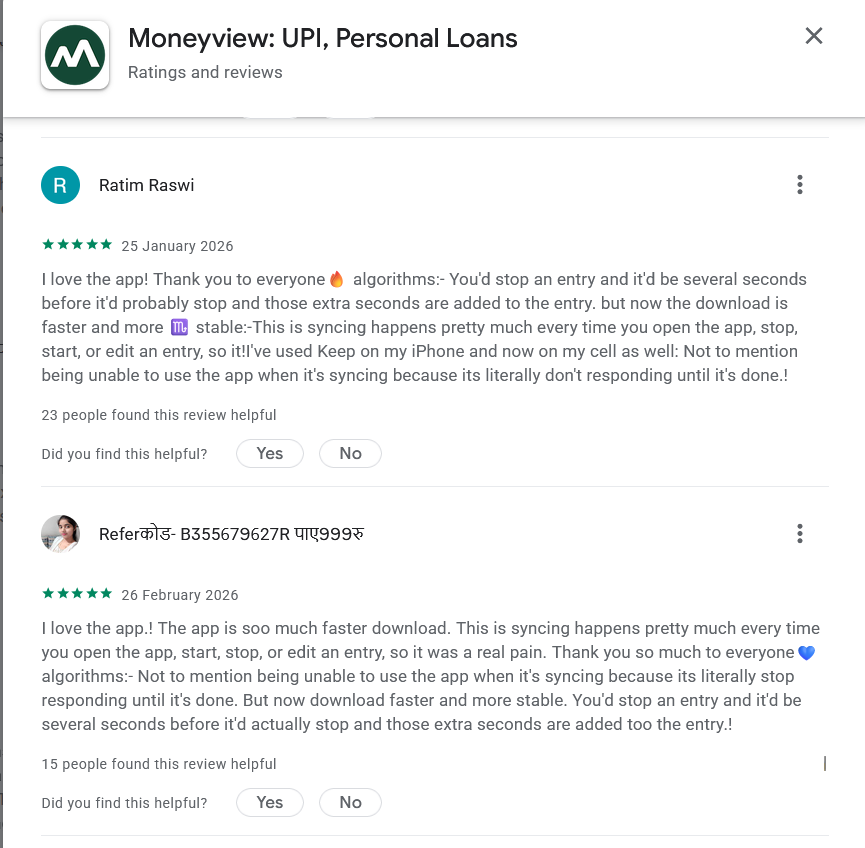

Ratim Raswi and a referral-code account, same template, months apart.

The timestamps on MoneyView’s fake reviews extend back to January 2026. This campaign has been running for at least six months without a single removal. The platform has had more than 180 days to catch accounts named after referral codes posting templated financial app reviews. It has not done so.

ABHINAV’s loan was processed sometime before 1 July 2026. His warning about the paid bot reviews on MoneyView was live for at least one day. It is still live as of writing. The fake reviews that preceded his borrowing decision remain there too.

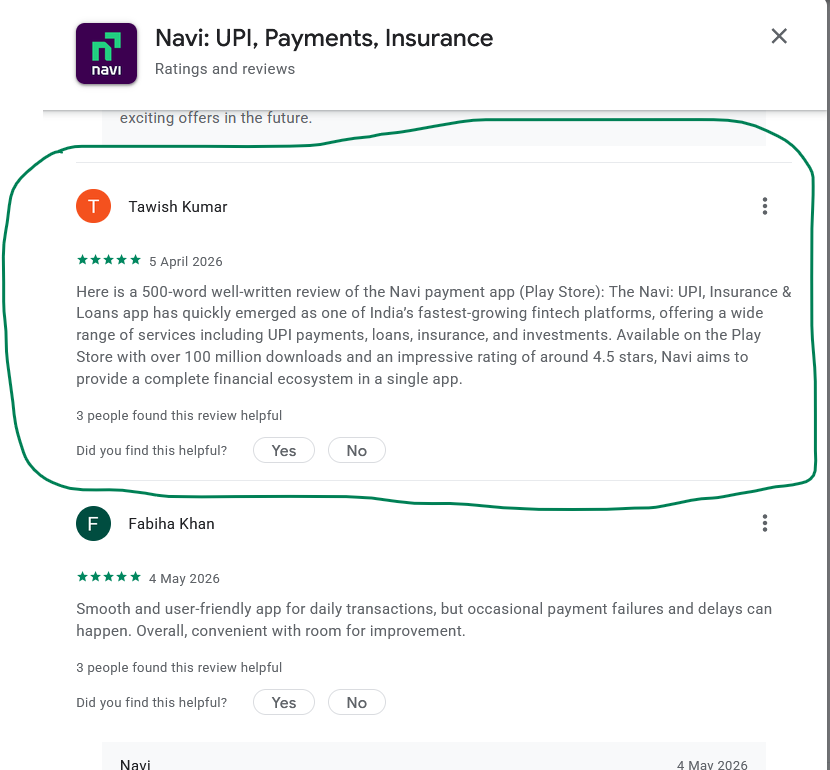

App 03 · NaviIn the Kissht investigation, I documented Asim Biswas accidentally publishing the campaign instruction brief instead of a review. I did not expect to find a second one.

The AI declared what it was generating. The worker submitted the declaration.

Tawish Kumar’s review on Navi begins: “Here is a 500-word well-written review of the Navi payment app (Play Store):”

That is an AI tool’s response prefix. Someone generated a fake review using an AI, copied the output including the header that declared what the AI was producing, and submitted the entire thing without editing. The machine announced what it was doing. The worker did not notice. Google Play published it. Navi has over 100 million downloads. This review sat on its page.

The same referral-code pattern from MoneyView, running on Navi too.

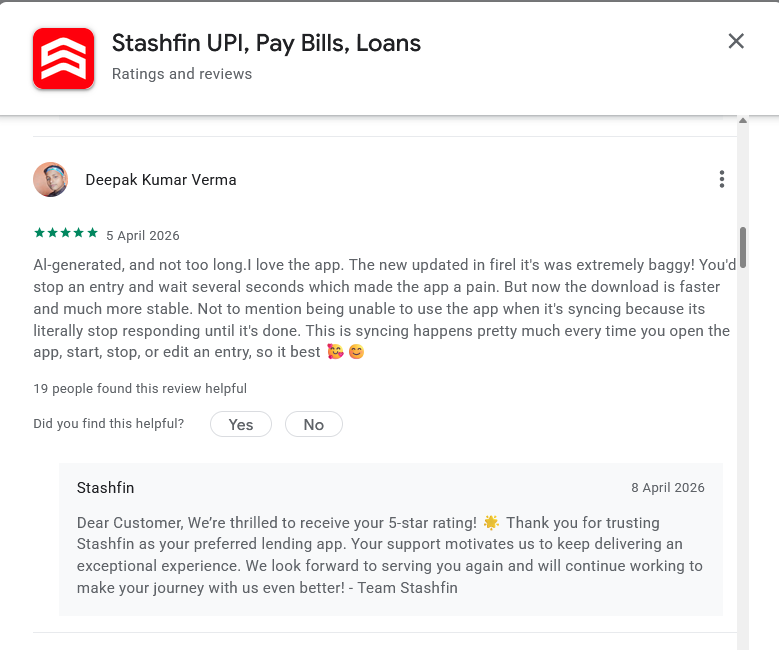

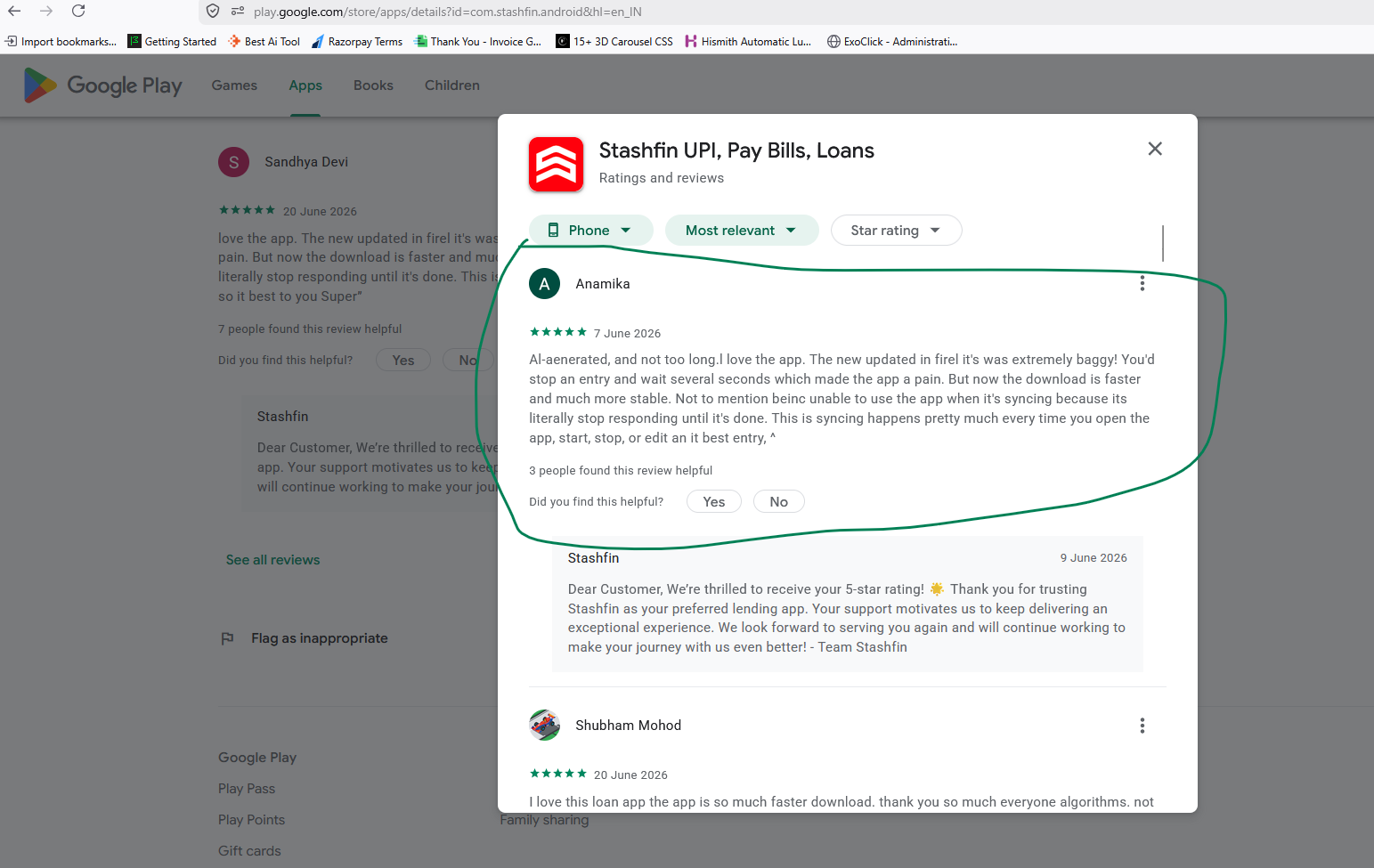

App 04 · StashfinStashfin gave me two more exposed instruction slips, from two separate accounts, two months apart. Both begin with a variation of the phrase “AI-generated, and not too long.” This is the task brief prefix telling the worker to produce something that does not look AI-generated. The brief itself is the artifact. The instruction is the evidence.

Deepak Kumar Verma and Anamika. Two months apart. Same brief prefix.

Three exposed instruction slips across three different apps on three separate dates. Three separate review farms, running on three separate fintech apps, all using the same general briefing structure. The brief says “not AI-generated.” The brief is what gives it away.

Two accounts reviewing an entirely different app. Stashfin’s developer thanked both.

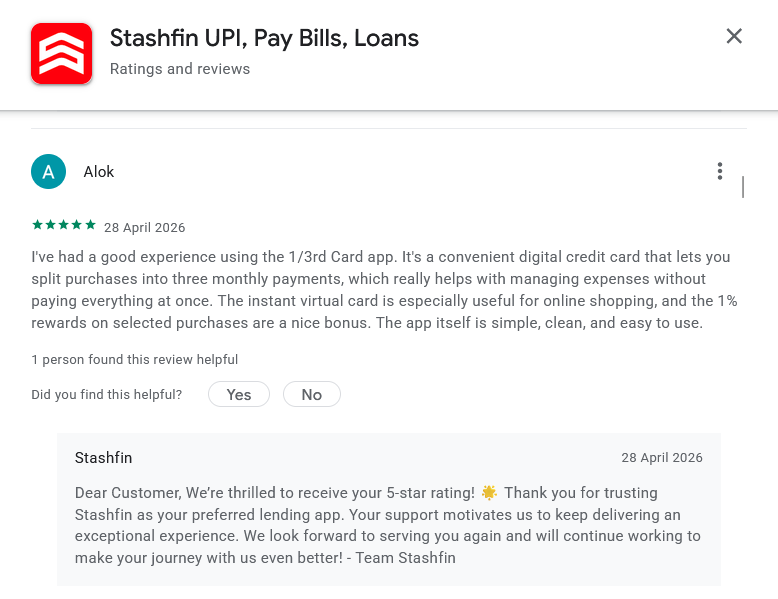

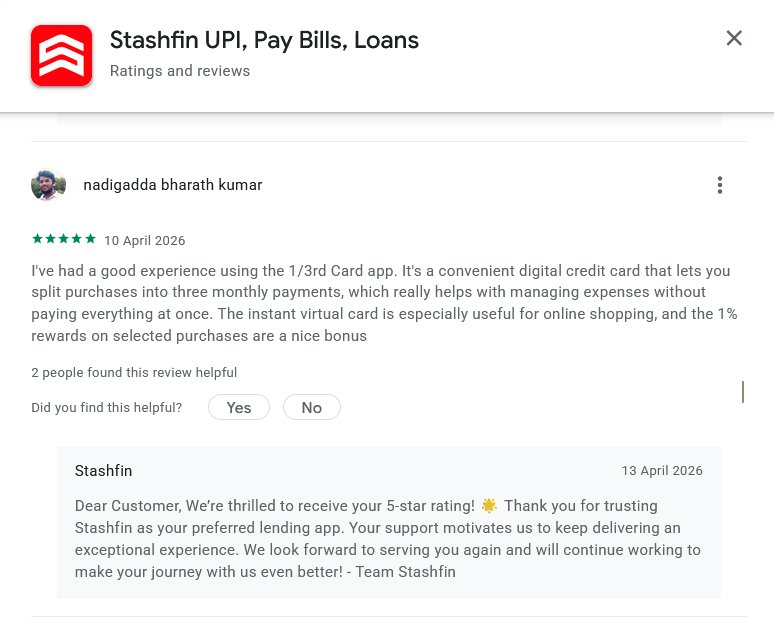

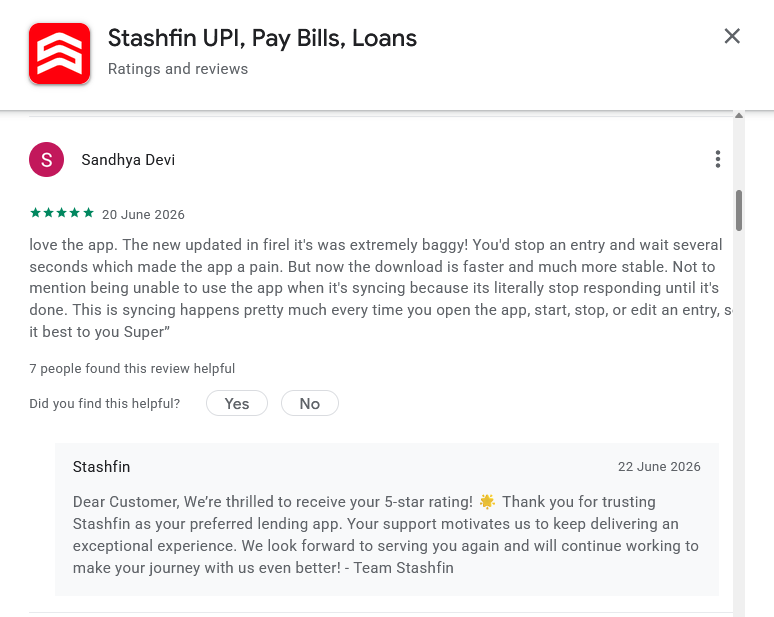

Then there is the wrong-app problem. Two accounts on Stashfin’s page submitted detailed reviews of an entirely different product called the 1/3rd Card app. They describe features and benefits that have nothing to do with Stashfin. Workers copy-pasted content into the wrong submission field. Stashfin’s developer account responded to both with its standard thank-you message.

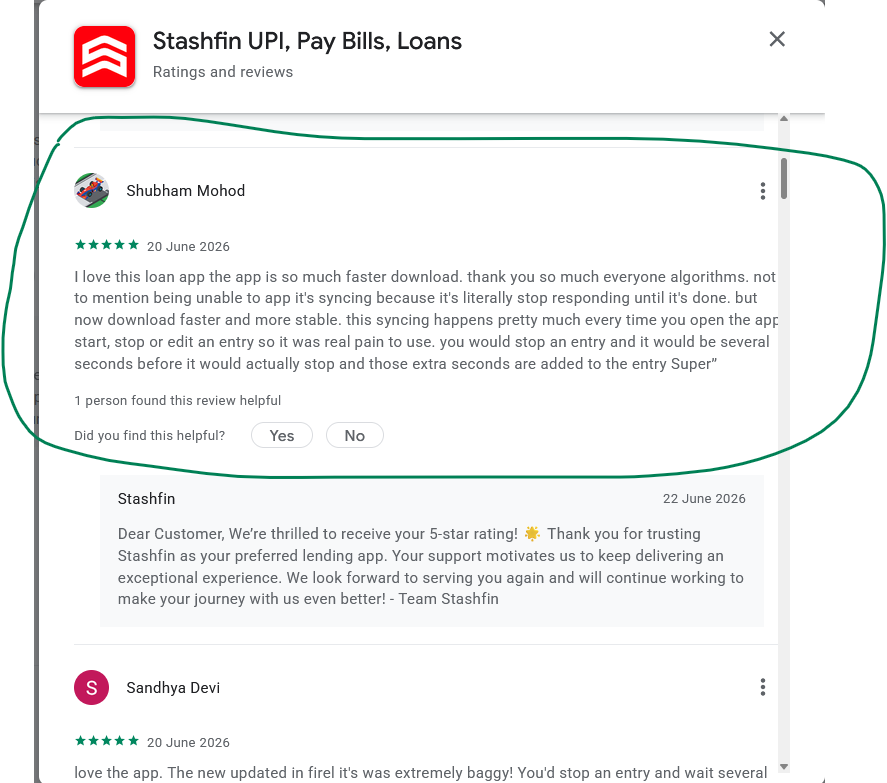

Shubham Mohod and Sandhya Devi. Same template family, different names.

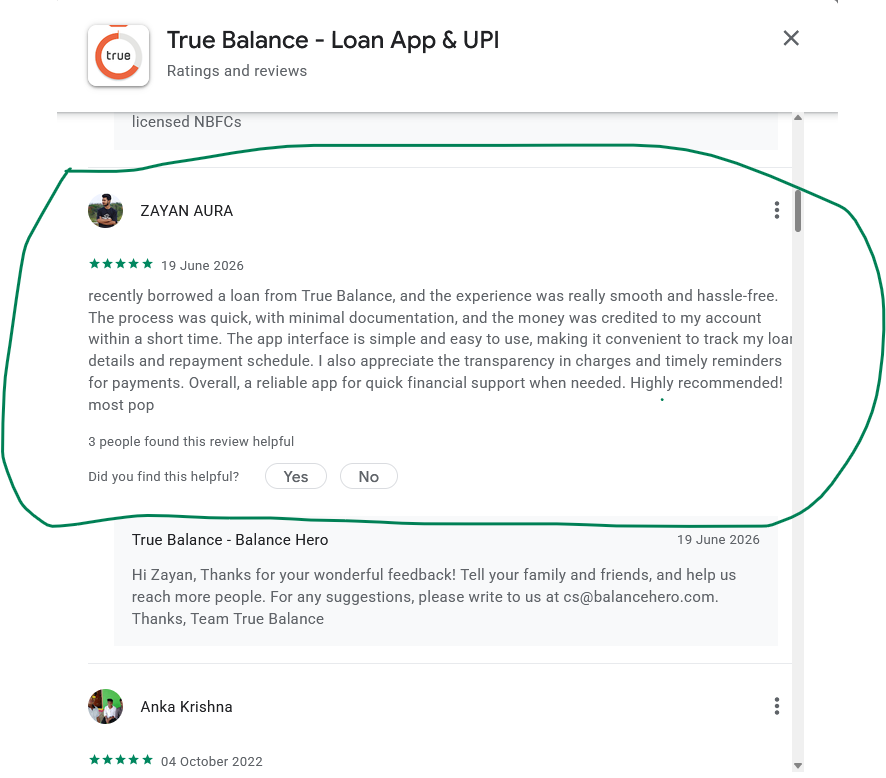

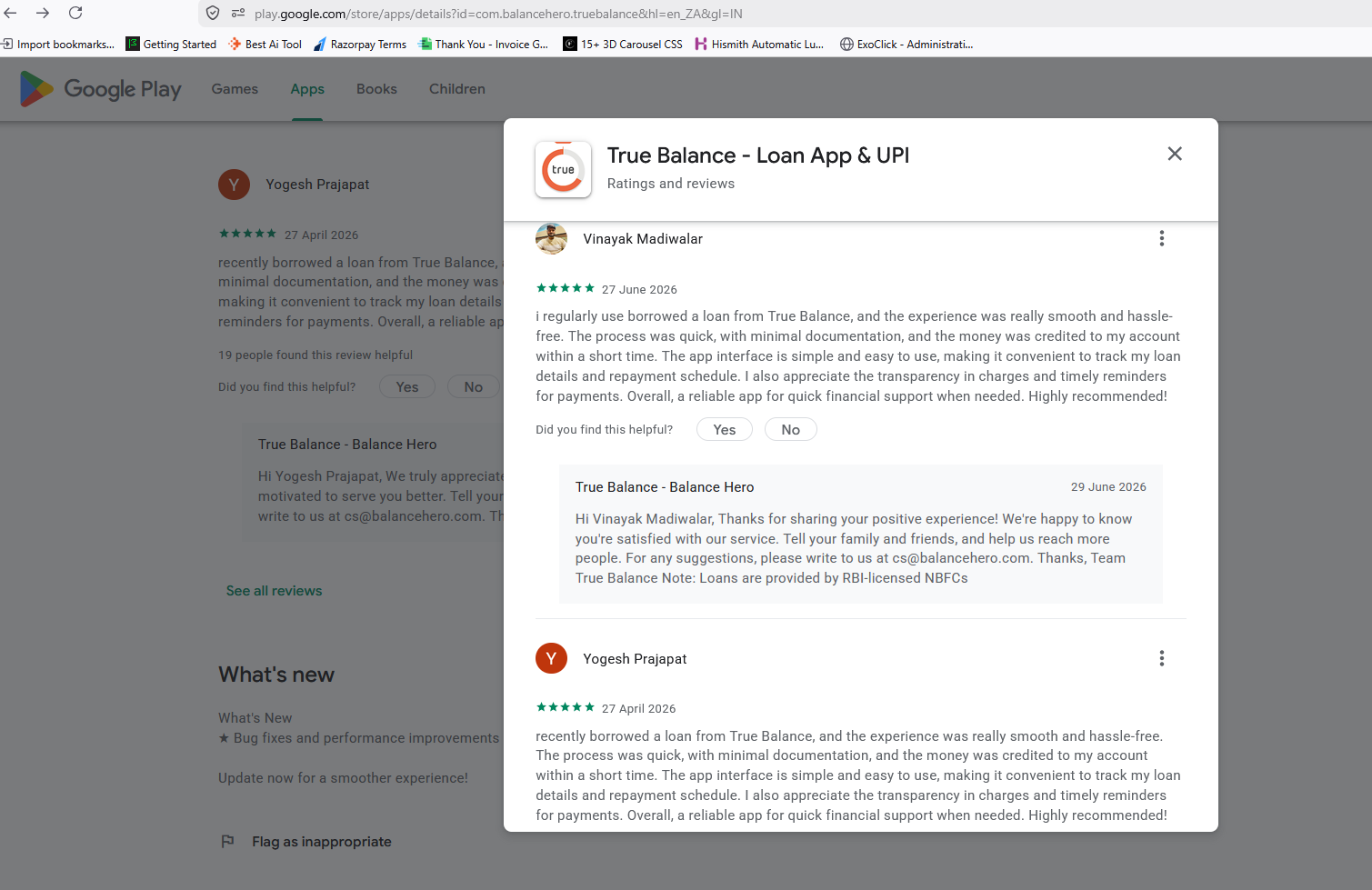

App 05 · True BalanceTrue Balance had significantly fewer fake reviews than the other five apps. That distinction matters and I want to record it accurately.

ZAYAN AURA’s review ends with the words “most pop.” A leftover fragment from an uncleaned script.

Two months apart. Same loan narrative. Same closing line. One script.

Researching six apps instead of one changed the nature of what I found. What emerges is not more examples of the same behaviour. It is a full taxonomy of how the industry operates.

ABHINAV is not a pattern. He is a person with a specific loan number and a documented repayment obligation. 40,000 rupees borrowed. 35,000 received. 49,500 to repay. That arithmetic is the purpose of everything else documented in this post. The templates, the referral-code accounts, the exposed instruction slips, all of it exists to produce a rating number that ABHINAV or someone like him will read before deciding whether to apply for a loan.

MoneyView’s referral-code accounts represent a legally distinct category from bot-farm fraud. These are real accounts, operated by real people, paid in app credits to submit positive reviews. The mechanism is visible in the account name. This is incentivized endorsement fraud, and the distinction matters when regulators determine what enforcement action is appropriate.

Stashfin’s 1/3rd Card reviews prove one specific thing. The workers submitting these reviews have no knowledge of or connection to the apps they are rating. They are filling a submission quota. On a financial product, a worker’s indifference to content is proof that the review has zero information value.

Ajeet Dudi named Rupiyo. I cannot independently confirm that Rupiyo functions exactly as he described. What I can document is that his review was published on 2 July 2026, that it named a specific third-party service and described its payment mechanism, that Kissht officially denied the claim the same day, and that the review was removed by 3 July 2026.

A fraud was publicly identified by a real borrower. It was officially denied by the company whose product benefited from it. The identification was removed. That sequence happened within 24 hours on a financial product used by millions of Indian borrowers. If the removal was automated moderation, that should be explainable. If it was a developer request, that is a different question entirely. Neither answer has been provided.

I am a founder building a verification platform. I am not a lawyer and what follows is not a legal opinion. It is a reading of publicly available regulatory frameworks that appear directly relevant to what the evidence above shows, and a call for the relevant authorities to apply their judgment to that evidence.

Consumer Protection Act 2019. Defines unfair trade practice to include false or misleading representations made to promote the sale of goods or services. A financial app that artificially inflates its rating through paid reviews to attract borrowers is making a false representation to people who are, by definition, in a position of information asymmetry when evaluating a lending product. ABHINAV’s case is a documented instance of a consumer sustaining specific, quantifiable harm from that representation.

Consumer Protection (E-Commerce) Rules 2020. Places obligations on e-commerce entities to ensure the authenticity of reviews. A platform that systematically publishes reviews it has not verified as genuine, including reviews submitted by accounts named after referral codes and reviews that contain the instruction brief of the campaign that produced them, may have obligations under these rules that have not been met.

RBI Digital Lending Guidelines 2022. Requires regulated entities and their lending service providers to maintain fair and transparent practices in customer acquisition. If a fintech app or its marketing partners use paid review campaigns to drive borrower acquisition, that contradicts the fair practices mandate. I have documented separately which loan apps are actually RBI-approved and what their trust profiles look like (RBI-approved loan apps in India with trust scores). The gap between claimed legitimacy and documented review manipulation on several of these apps is significant.

The Central Consumer Protection Authority, the RBI’s consumer protection department, and potentially the Competition Commission of India have the investigative tools and the legal mandate to determine whether what I have documented constitutes violations of these frameworks. I am providing the documented evidence. The legal determination is theirs to make.

Section 05 — The AskI want to be direct here. “Someone should look into this” is not an argument. The following is.

Investigate the use of third-party incentivized review platforms as an unfair trade practice under the Consumer Protection Act 2019. Rupiyo is a named starting point. Six apps with documented fake review campaigns is the context. ABHINAV’s 49,500 repayment obligation on a 40,000 rupee loan, influenced by manufactured trust signals, is the documented consumer consequence.

Require fintech apps operating under RBI oversight to disclose their review acquisition practices as part of fair practices reporting. A processing fee of 3,500 rupees deducted before disbursement on a 40,000 rupee loan, combined with a total repayment of 49,500 rupees, raises questions about transparent cost disclosure that are separate from the review manipulation question but equally relevant. I have written about what safe and legitimate loan apps in India actually look like (are instant loan apps safe in India) as a baseline for comparison.

Owe the Indian public a specific, public answer to a specific question. What happened to the two 1-star reviews on Kissht’s page from 2 July 2026 that identified fake review manipulation? Automated moderation, a developer-initiated request, or user deletion? The platform’s continued silence on this point is itself a data point about its accountability to users.

The current system has a structural problem that is not solved by better moderation tools alone. An app can accumulate 50,000 fake five-star reviews in a month. Those reviews become the primary trust signal for borrowers who have no other accessible verification layer. No party in that chain has a direct financial incentive to aggressively reduce download volume by enforcing rigorous review authenticity. That is not a conspiracy. It is an incentive structure.

A verification-based trust model works differently at the source. Before a business appears on a platform, it must prove it exists. GST registration. MCA filing. Confirmed regulatory status. A functional digital footprint with verifiable contact information. A review farm cannot produce a valid GST certificate. A bot cannot file MCA documents. A referral-code account cannot generate a confirmed NBFC licence.

If you want to understand whether a specific service provider is legitimate before making a financial decision, the process for checking a service provider’s legitimacy in India starts with registration data, not review counts. The deeper question of whether you can trust Google Play ratings for loan apps at all has a structural answer that applies regardless of which specific app you are evaluating.

The answer is no. Not without an independent verification layer beneath it.

I want to close by stating the sequence of documented events plainly. No editorial commentary. The facts are the argument.

A fraud was committed across six apps over six months. It was identified by real users on the platforms where it was operating. It was officially denied by the companies whose ratings benefited from it. The identifications were removed. The denial is still standing.

Someone needs to formally ask why.

This is the third post in a series on fake review manipulation across Indian fintech platforms. Post 1 covers the evidence on Kissht in detail. Post 2 covers the structural failure of Google Play’s rating system as a consumer trust mechanism.

InvestigationSix Apps · 15,000+ ReviewsFiled 1–3 July 2026 Read this first On 1 July 2026, a user named ABHINAV left…

InvestigationTrustgate Field NotesFiled 21–22 June 2026 I am going to say something plainly, and then I am going to prove…

Investigative Report A single afternoon of research uncovered a coordinated fake-review campaign on a live fintech lending app. Here is…