Paid, Planted, and Silenced: How a Named Review Farm Is Running Unchecked Across India's Top Fintech Apps

InvestigationSix Apps · 15,000+ ReviewsFiled 1–3 July 2026 Read this first On 1 July 2026, a user named ABHINAV left…

I am going to say something plainly, and then I am going to prove it. Google Play’s star rating system is not an independent measure of quality. It is a number that any sufficiently funded operation can purchase, inflate, and maintain without detection. Calling it a “rating” implies that something is being independently measured. Nothing is being independently measured. What you are looking at, every time you see 4.5 stars and 50,000 reviews on a financial app, is the output of whoever spent the most on submissions.

I did not arrive at this conclusion from theory. I arrived at it from screenshots.

Before naming the failure, name the incentive. This is important context, and most people skip it.

Google Play takes a commission of 15 to 30 percent on in-app purchases and transactions processed through its platform. That commission is directly tied to download volume. More downloads generate more in-app transactions. More transactions generate more commission revenue for Google.

A higher star rating drives higher download volume. That is not speculation; it is documented consumer behaviour across every app marketplace that has ever published data on the relationship between ratings and install rates.

Google Play is therefore not a neutral arbiter of app quality. It is a marketplace with a direct financial stake in high download numbers, and high download numbers are produced by high ratings. These two facts sit alongside each other without anyone at the platform being corrupt or deliberately negligent. The problem is not bad intent. The problem is a structural misalignment between what the platform earns and what rigorous moderation would cost it.

That misalignment has consequences. The evidence below shows what they look like in practice.

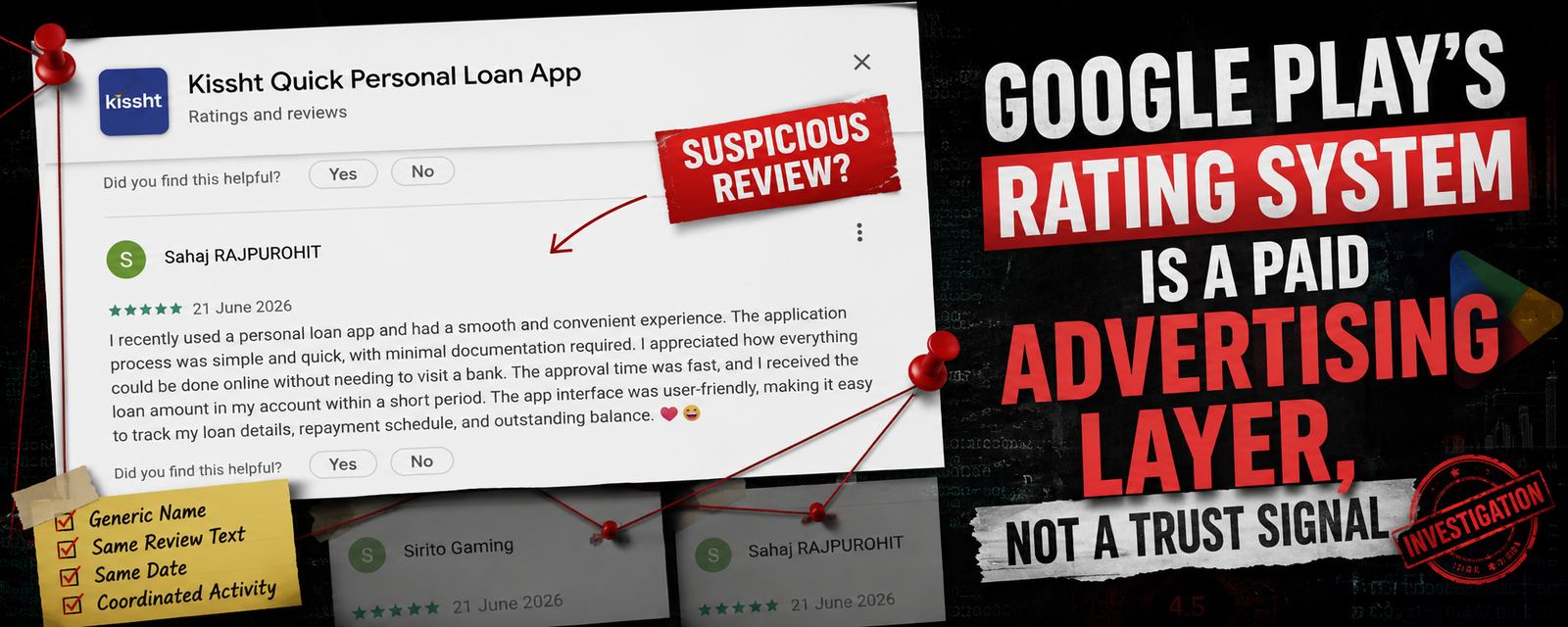

Section 02 — The EvidenceI was cross-referencing reviews on a live personal loan app on Google Play when I found this. I was not running an investigation. I was browsing for a few minutes. This is what was sitting on the surface.

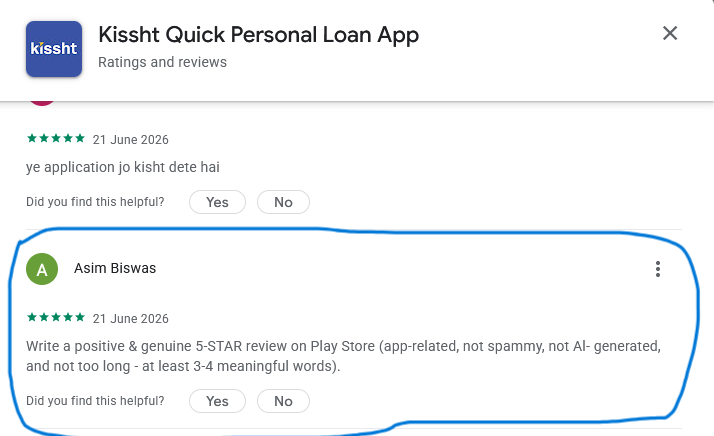

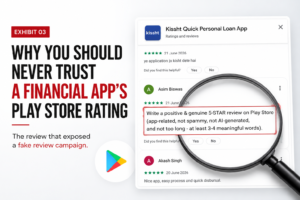

This review was never written. This was the purchase order. Asim Biswas did not describe an experience. He published the task brief he was given.

The user “Asim Biswas” did not leave a review. He published the task brief he was given by whoever was running the campaign. The text reads: “Write a positive and genuine 5-STAR review on Play Store (app-related, not spammy, not AI-generated, and not too long, at least 3-4 meaningful words).”

That is a purchase order. Someone paid for reviews. A worker received the instruction, forgot to replace it with the actual output, and submitted the brief itself as the review. Google Play published it. It remained live. It was never removed or flagged.

That is not a moderation error. The word “error” implies a process that tried and failed. This is the absence of a process.

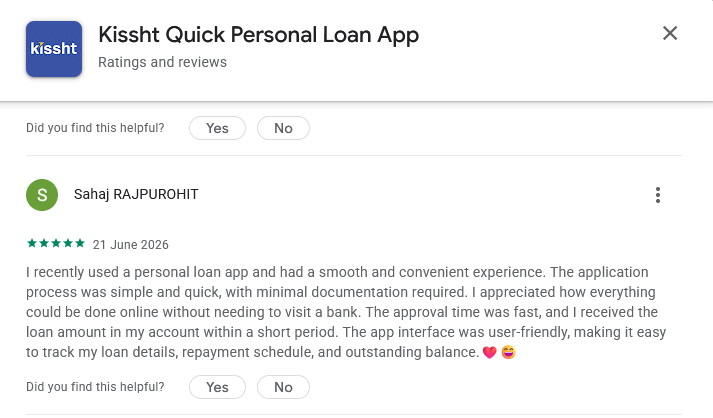

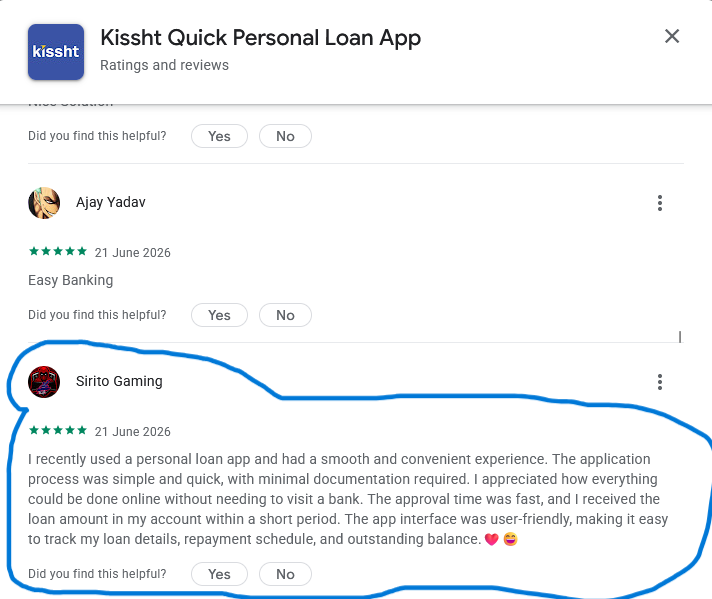

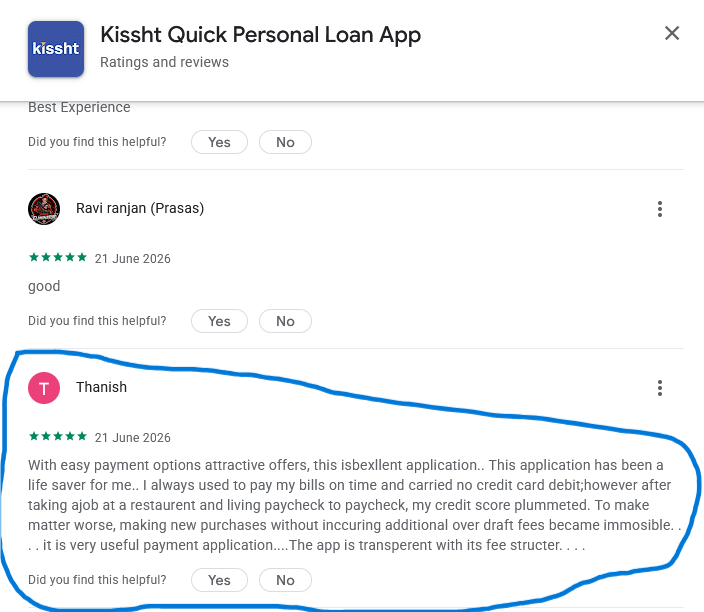

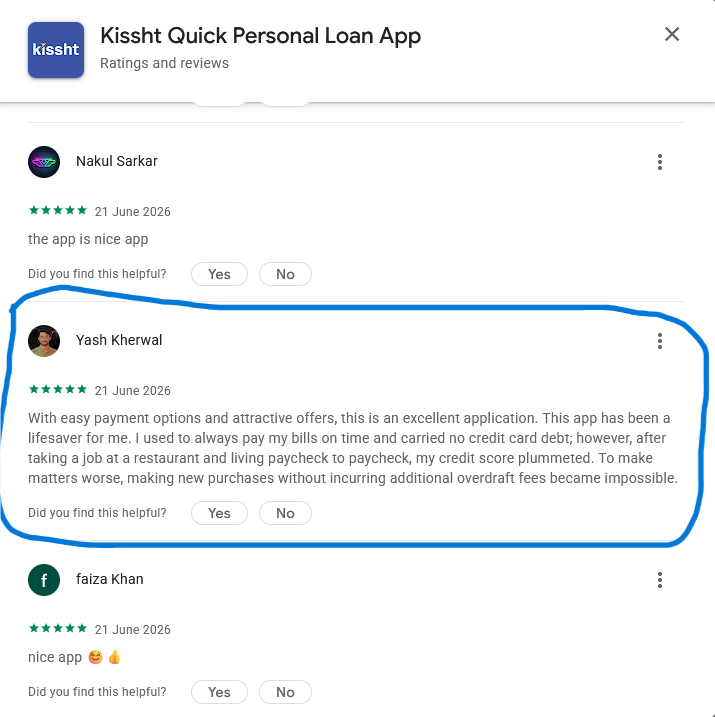

Exhibit B. Two accounts. One script, down to the emojis. Google Play read both submissions and published both as authentic feedback.

These are two separate accounts. The review is identical. Not similar. Not paraphrased. The same sentences, in the same order, with the same emojis in the same positions. Google Play’s moderation system looked at both of these submissions and published them both as authentic user feedback.

Section 03 — The Defence, DismantledWhen platforms are confronted with moderation failures of this kind, the defence is always scale. Billions of data points. Millions of reviews. No system is perfect.

I understand the scale argument. I am rejecting it here, specifically, because the failures I documented do not require sophisticated detection. They require basic detection, and that basic detection was absent.

Consider what it would have taken to catch the Asim Biswas submission. One human reading one sentence. The text of the review is literally the instruction to write a fake review. The phrase “Write a positive 5-STAR review on Play Store” is not ambiguous content that requires judgment to evaluate. It is a transparent declaration of fraudulent intent. Any keyword filter built in the last fifteen years would have flagged it instantly. It was not flagged. It was published.

Now consider the date clustering across every account I documented.

Five different accounts. One afternoon. Let the repetition make the argument.

Every single review I captured carries the same date: 21 June 2026. Fifteen-plus five-star reviews submitted by different accounts in a single afternoon on a single app is a statistical anomaly that any automated system designed to catch coordinated inauthentic behaviour would surface as a priority flag. Coordinated review campaigns are one of the most well-documented forms of platform manipulation. The detection methodology for them has existed for years.

The campaign ran, completed, and sat published without a single intervention.

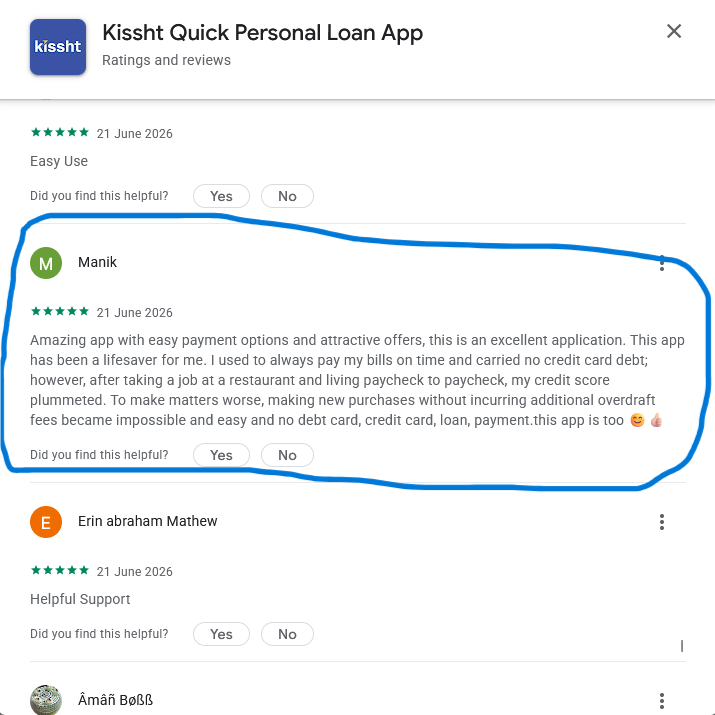

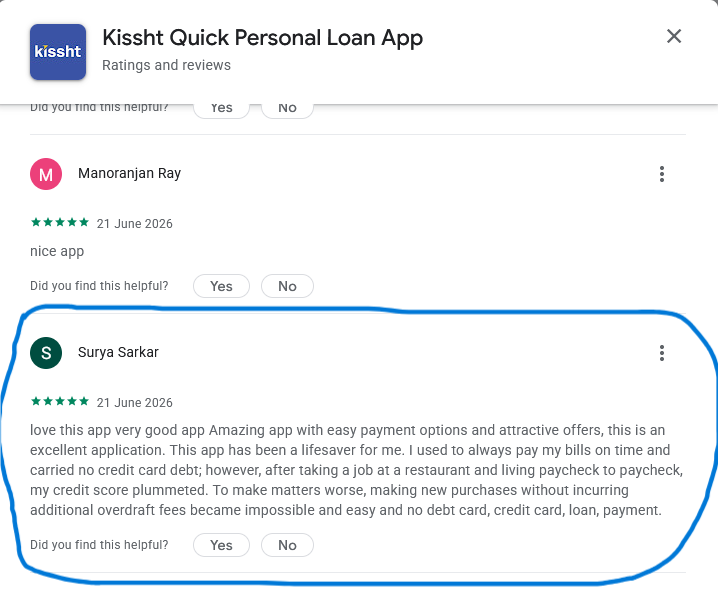

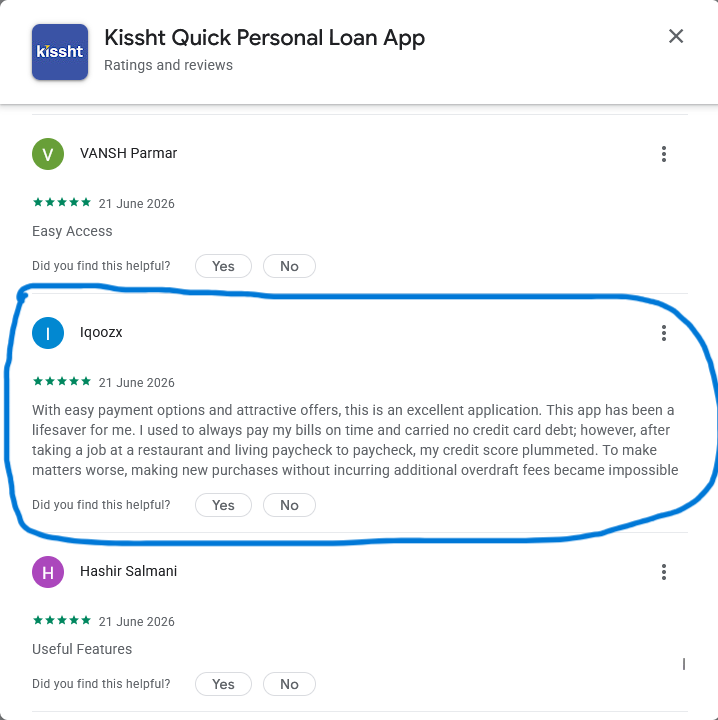

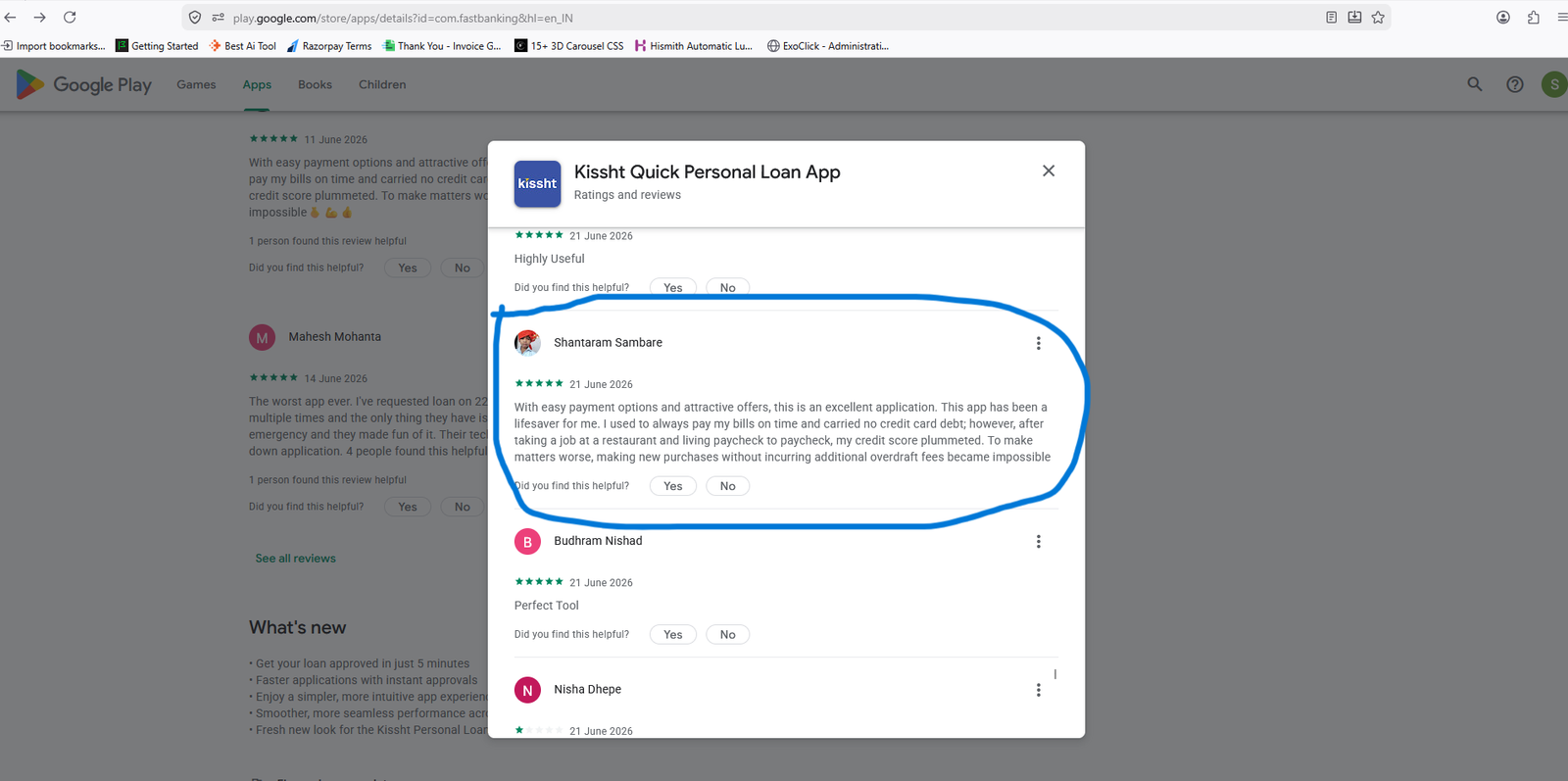

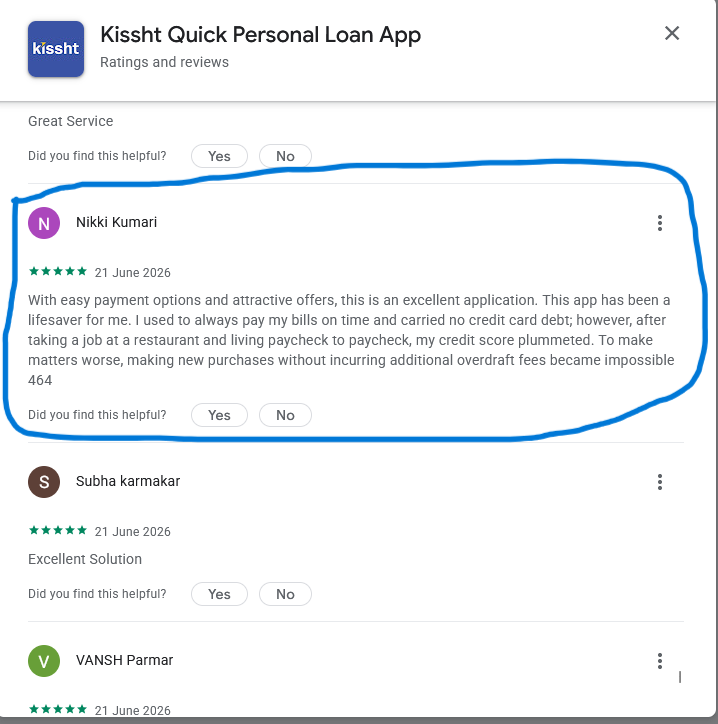

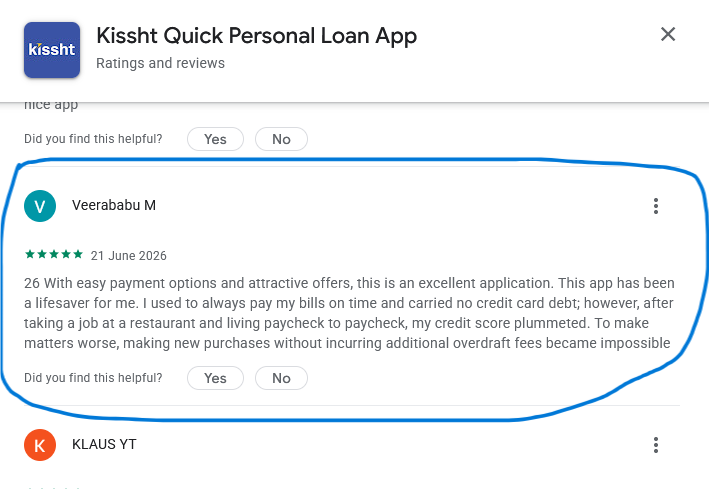

The “restaurant and credit score” template paragraph appearing across more than a dozen accounts is a third failure. The same core paragraph, word for word, submitted by accounts with no other review history, spread across a single afternoon. A string-matching algorithm running on any standard content database would flag this in milliseconds. It is not a needle in a haystack. It is the same needle, submitted repeatedly, from accounts that had no other activity.

These were not hard to catch. They were simply not caught.

The difference between those two things matters when the app in question is a personal loan product that millions of users are evaluating before granting access to their bank accounts and financial data.

Section 04 — The Human CostThe structural argument about platform incentives and moderation failures is important. But the human cost is what makes it urgent.

The population most harmed by fake reviews on loan apps is the population least equipped to absorb that harm. People searching for a personal loan app on Google Play are, by definition, often under financial pressure. They need money quickly. They are making a fast decision. And in the absence of any other accessible verification layer, a 4.5-star rating from 50,000 apparent users functions as their primary trust signal.

That trust signal was manufactured.

The account has no connection to the content. The platform has no mechanism to check. The user reading this review has no way to know.

This account’s profile picture has no plausible connection to the content it posted. The review describes adult financial hardship in specific detail: a restaurant job, living paycheck to paycheck, a plummeting credit score, mounting overdraft fees, the exact template circulating across the other accounts above. It is a junk account, a purchased throwaway, or a stolen profile given one job: submit the template.

The platform has no mechanism to verify that the person rating a financial product has any relationship to that product. The user reading the review has no way to know the account is unconnected to the experience being described.

This is not an edge case. This is the operating standard of an unverified review system applied to financial products. I have covered the question of whether instant loan apps are actually safe in India in detail elsewhere. The short answer is that safety cannot be assessed from a star rating. It requires verification at the entity level, not aggregation at the review level.

Section 05 — The DistinctionThis is the core distinction that the current app store model collapses, and consumers pay the price for that collapse.

A rating is an aggregate of submissions. It can be manufactured at scale, as the evidence above demonstrates. The process for inflating a rating is well understood, widely available, and not particularly expensive. A coordinated campaign of the kind I documented can be executed in a single afternoon.

A credential is a verifiable claim tied to a real entity with real accountability attached to it. A GST registration. An MCA filing. A confirmed NBFC licence from the RBI. A functional registered address. These are claims that require a real business to stand behind them. They cannot be faked by submitting text to a database.

A trust signal should function like a credential. On Google Play, it functions like a rating. These are not the same thing, and presenting one as if it were the other is precisely what makes the current system dangerous in the context of financial products.

The question of whether you can trust Google Play ratings for loan apps deserves a structural answer, not just a case-by-case warning. The structural answer is: no, not without an independent verification layer beneath it.

Section 06 — The AlternativeThe reason fake review campaigns work on Google Play is not that the bots are sophisticated. It is that there is nothing behind a listing that requires proof of existence. An app can be published, rated, and downloaded by millions of users without the company behind it ever having to demonstrate that it is legally registered, financially regulated, or operating within the boundaries that the RBI requires of lending entities.

A verification layer changes this at the source.

When a business must produce a valid GST registration, a confirmed MCA filing, and a transparent digital footprint before it is approved for listing, the entire category of bot-farm manipulation becomes structurally irrelevant. Bots cannot produce a valid GST certificate. A review farm cannot generate a confirmed NBFC licence. The verification requirement filters out the class of bad actor that fake reviews are designed to serve.

This is not a complex technical solution. It is a decision about what the minimum requirement for listing should be. On TrustGate, that minimum is verifiable identity. On Google Play, that minimum is a working internet connection.

If you want a baseline of which lending platforms have passed that verification threshold, the RBI-approved loan apps in India with trust scores I maintain on TrustGate represents a starting point built on registered credentials rather than submitted text. The same principle applies to any digital service provider, which is why I also cover how to check if a service provider is legitimate in India as a general framework.

“Nikki Kumari” ends her review with the number 464. “Veerababu M” begins his with the number 26. These are not typos. They are production errors left behind by automation scripts that nobody cleaned before submission. They survived moderation because there was no meaningful moderation to survive.

A Google Play star rating on a financial app tells you one thing: someone spent money on submissions. It tells you nothing about whether the company is real, whether it is regulated, whether it holds the licences that Indian law requires of entities that lend money to consumers.

Before downloading any financial app, verify the entity behind it through a source that requires proof of registration, not just the ability to submit text. Whether that means checking best instant loan apps in India for 2026 through a verified directory, or cross-referencing the app developer’s credentials against RBI and MCA records directly, the process is the same.

Demand proof of identity.

Not a star count.

The 4.5 stars you are looking at were not earned by satisfied customers. They were ordered on the same afternoon, by the same operation, from the same template. And the platform that published them earns a commission every time someone downloads the app those stars are attached to.

Call it what it is.

InvestigationSix Apps · 15,000+ ReviewsFiled 1–3 July 2026 Read this first On 1 July 2026, a user named ABHINAV left…

InvestigationTrustgate Field NotesFiled 21–22 June 2026 I am going to say something plainly, and then I am going to prove…

Investigative Report A single afternoon of research uncovered a coordinated fake-review campaign on a live fintech lending app. Here is…